You may have the question at some point: how to build business credit fast without risking personal assets or wasting months on guesswork.

The process follows a clear order. Skip a step and everything after it slows down. Follow the order.

A client hired me who had a print-on-demand apparel store in 2019 with zero business credit history.

His first supplier financing request got denied because the lender could not separate his finances from his company’s.

That denial pushed him to build the system the hard way. I want to save you that pain.

How to Build Business Credit Fast

So, want to build business credit fast? Start with the legal foundation. Form an LLC, grab your EIN free from the IRS, then open a dedicated business bank account.

Next, request a free D-U-N-S number from Dun & Bradstreet right away. Every week you wait is history you lose.

Open two or three vendor accounts that report payments, and pay invoices early, not just on time.

Add a business credit card and keep usage under 30%. Check all three bureaus a few times a year for errors.

This sequence builds a lendable profile in 12 to 24 months, with real movement showing in 3 to 6 months.

Short Checklist to Build Business Credit Fast

- Form an LLC or corporation

- Get your EIN free through the IRS

- Open a dedicated business bank account

- Apply for a D-U-N-S number right away

- Open two or three net-30 vendor accounts that report

- Add a business credit card and keep utilization under 30%

- Pay every invoice early, not just on time

- Check all three bureaus several times a year

- Stay patient. Twelve to twenty-four months builds a lendable profile

No shortcuts exist, but discipline beats speed every time. I’ll explain the steps in detail. So, you can go on reading.

The Value of Business Credit for Sellers

Sometimes you may face a unique cash flow problem. Inventory gets ordered weeks before it sells.

Ad spend hits your card before revenue comes in. Software subscriptions stack up monthly.

86% of firms now use financing regularly, with credit cards and loans as the most common products.

Sixty percent of firms applied for financing in the past year, mostly to cover operating costs or grab a growth opportunity. Fedsmallbusiness

That gap between spending and selling is exactly why business credit matters.

Lenders decide who gets approved based on the credit profile tied to your business, not your personal score.

Your First Seven Moves to Build the Foundation

Most online sellers jump straight to applying for credit. That order backfires. Business credit follows a structure, and each piece locks the next one into place. Skip one, and the whole chain weakens.

These seven steps lay that structure down, brick by brick. Some take a few minutes. Others take weeks to process.

Run through them in order, and your business builds a credit identity that stands apart from your personal name.

Step 1: Set Up Your Online Business as a Separate Legal Entity

You cannot build business credit fast as a sole proprietor, even if your entire operation runs through a Shopify store or an Etsy shop.

Lenders tie sole proprietorships to your Social Security number, not a business profile.

Register your company as an LLC through your state’s Secretary of State office.

This creates legal distance between you and your business, whether you are selling skincare products you manufacture or running a digital course platform.

Quick checklist:

- Choose a business name and check availability

- File formation documents with your state

- Pay the state filing fee

- Get a dedicated business address (some banks reject virtual addresses, which matters if you run a fully remote ecommerce brand)

Step 2: Get Your EIN the Same Day

Your Employer Identification Number works like a Social Security number for your company.

You need it to open a bank account, file taxes, and apply for credit, even if your only storefront is a website.

Apply directly through the IRS website. It is free and takes minutes online. Never pay a third party for this.

I have seen new dropshipping owners pay $75 for something the IRS hands out at no cost.

Step 3: Open a Business Bank Account and Keep It Separate

A dedicated business checking account does not show up on your credit report directly.

But it builds banking history that lenders check before approving financing. This matters for online sellers because payment processors like Stripe or PayPal deposit straight into this account. Lenders want to see that flow clearly separated from personal spending.

Keep every business expense, including ad platforms, packaging suppliers, and software tools, running through this one account.

Step 4: Get a D-U-N-S Number From Dun & Bradstreet

This is the step most online sellers miss, and it costs them months.

A D-U-N-S number is a nine-digit ID that Dun & Bradstreet uses to track your company’s credit activity.

Without one, your business has no profile with D&B, the bureau most lenders pull first for your PAYDEX score.

Request it free through the dnb.com website. Standard processing runs close to 30 days, though an expedited option exists for a fee.

Apply the same week you get your EIN, even if your business only sells digital downloads or printables.

Step 5: Open Trade Lines With Vendors That Report

This is where business credit actually starts moving. It looks different depending on what you sell online.

Run a physical product store? Your trade lines come from packaging suppliers, raw material vendors, or fulfillment companies. Most offer net-30 terms.

Run a digital business, like a SaaS tool or an online course platform? Trade lines often come from hosting providers and software vendors.

Ship anything physical at all? Add freight and print partners to that list. Either way, confirm with each vendor that they report to a bureau before opening the account.

Pay every invoice 10 to 15 days early. Dun & Bradstreet’s PAYDEX score rewards early payment more than on-time payment.

This single habit moved my client’s print-on-demand brand’s PAYDEX score from nothing to 80. It took just four months. All from paying his blank apparel supplier ahead of schedule.

Step 6: Add a Business Credit Card

Once you have one or two trade lines reporting, apply for a business credit card.

Cards report to bureaus faster and more consistently than most vendor accounts. They cover the daily spend that online businesses rack up fast: ad campaigns, app subscriptions, shipping labels.

Keep your usage below 30% of your limit. Pay the statement in full every month.

A friend runs a candle business on Shopify. During a holiday ad push, she ignored her credit utilization for two months.

Her score dropped ten points in one cycle. She fixed it fast. She started paying down her balance twice a month instead of once. One small habit. One big difference.

Step 7: Monitor All Three Bureaus

Business credit bureaus do not always agree with each other. Each one can hold different information about your company.

| Bureau | Score Name | What It Tracks |

| Dun & Bradstreet | PAYDEX | Payment speed (early vs. late) |

| Experian Business | Intelliscore Plus | Payment history, public records, credit usage |

| Equifax Business | Business Credit Risk Score | Payment trends, credit utilization, business size |

Check all three bureaus a few times a year. Errors show up more often than owners expect. Business scores are public, too.

A small mistake can quietly cost an online seller their vendor terms before they even notice. Free basic reports exist. Full reports usually cost $50 to $200 per bureau.

How Long Does It Mostly Take?

There is no shortcut that skips time completely. But the timeline depends almost entirely on how fast you stack the steps above.

- Months 1 to 2: Entity formed, EIN secured, D-U-N-S applied for, bank account open

- Months 2 to 4: First trade lines reporting, first credit card approved

- Months 4 to 6: Active PAYDEX score, Experian and Equifax profiles populating

- Months 12 to 24: Strong enough profile for unsecured lines of credit or larger inventory financing

A strong credit profile takes time. Most lenders want to see 12 to 24 months of consistent, positive payments across multiple accounts.

There’s no shortcut around this part. It applies to online brands just as much as brick-and-mortar ones.

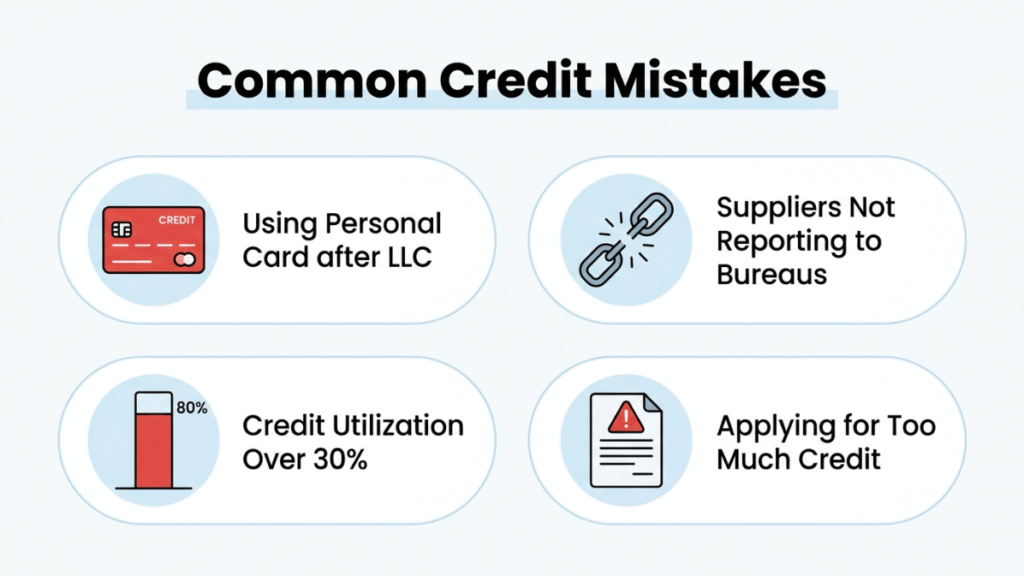

Common Mistakes That Slow Everything Down

- Continuing to use a personal card for ad spend or supplier orders after forming an LLC

- Choosing dropship suppliers without confirming they report to bureaus

- Letting credit utilization creep past 30% during a big sales push

- Ignoring credit reports until a supplier financing application gets denied

- Applying for too much credit at once, which signals risk to lenders

My best friend Jessica made this mistake in her first year running her ecommerce skincare line.

Sales slowed one month, and she treated her business card like a safety net. The balance sat near 80% of her limit for two months straight.

Her score dropped fast. Her packaging supplier noticed too and shortened her terms from net-30 to net-15.

It took five months of clean, on-time payments before she won that trust back.

Compare the Fastest Credit-Building Methods

No single method covers every bureau on its own. A mix of two or three, run with discipline, builds a complete profile fastest, no matter what you sell online.

| Method | Speed to Start | Reports to Bureaus? | Best For |

| Net-30 vendor accounts | 1 to 4 weeks | Often, confirm first | New stores with physical inventory |

| Business credit cards | 2 to 6 weeks | Usually yes | Covering ad spend and software bills |

| Business line of credit | 1 to 3 months | Usually yes | Seasonal inventory or ad budget swings |

| Trade references | Immediate | Indirect | Vouching for a new online brand |

Why Sequence Matters

A client of mine launched a digital planner and journal brand. She sold printable PDFs and printed versions through a small fulfillment partner.

She skipped the D-U-N-S step for almost a year. She thought it was optional paperwork.

Then she applied for inventory financing to print a larger run. The lender pulled her D&B file.

It was empty. She had nine months of perfect supplier payments. None of it counted toward her PAYDEX score.

Her D&B profile never existed in the first place. That one missed step cost her almost a year of progress.

Conclusion

Business credit rewards consistency over cleverness. There’s no secret trick here.

Just follow each step in order. Pay early every time. Check your reports before a lender does it for you.

Start today. By next year, your online business can stand on its own financial footing.

It will be separate from your personal credit. Ready for whatever growth comes next.

FAQ

Can a fully online business with no physical office still build business credit?

Yes. Bureaus track your EIN and business activity, not whether you have a storefront. A virtual office or home-based LLC works fine, as long as your bank accepts the address you register.

Do payment processors like Stripe or PayPal report to business credit bureaus?

No. Processors handle payments, not credit reporting. You still need vendor accounts, credit cards, or lines of credit that report directly to Dun & Bradstreet, Experian, or Equifax.

Will a personal credit card used for business expenses ever help build business credit?

No. Personal cards report to personal credit bureaus only. Even daily use for ad spend or supplies will not move your business score forward.

What if my online store has no inventory at all, like a digital product business?

Trade lines can come from software vendors, hosting companies, or freelance service providers instead of physical suppliers. The bureau reporting rule is the same either way.

Does a business credit score affect approval for ad spend financing or revenue-based funding?

Yes. Many revenue-based lenders for ecommerce and digital brands pull a business credit report alongside bank statements before setting terms.

Can a single-member LLC running a side hustle still qualify for net-30 vendor accounts?

Yes, in most cases. Vendors care more about a registered entity and an EIN than employee count or revenue size, especially for starter accounts.

Aliza Khatun is a Digital Marketing Professional and the founder of DigiGenHub. She has helped various businesses grow their online presence through real-world experience in marketing, branding, traffic growth, and business strategy.

Through DigiGenHub, she shows how to build and grow a business from the ground up using Website Setup, SEO, Branding, Paid Promotion, and smart digital tools.

She also highlights how AI can be used to its full potential to make content creation, automation, marketing, and business growth faster and smarter.

She believes that the right knowledge, modern technology, and the right tools can help any individual or business build a stronger online presence.