Setting up a business requires a clear plan to collect revenue. Modern buyers rarely carry cash. Most consumers in the United States prefer plastic or digital wallets.

So, learning how to receive credit card payments is the fastest way to grow your sales.

How to Receive Credit Card Payments

Learning how to receive credit card payments requires an organized infrastructure. This handles commercial transactions safely.

You must evaluate your monthly revenue to choose between a shared payment aggregator or a dedicated merchant account.

Operating above a twenty-thousand-dollar monthly threshold makes an interchange-plus fee structure the most cost-effective path.

To maximize profit margins, you should use secure payment links for remote transactions.

Submit deep data tracking for corporate accounts as well. These steps actively qualify transactions for lower wholesale interchange tiers.

Implementing advanced tokenization protects sensitive customer accounts. It satisfies strict data security standards.

By matching transaction processing methods to your actual sales volume, your business can lower card overhead costs.

This prevents unexpected account holds. Prioritizing modern processing mechanics keeps cash flow completely predictable. It provides a smooth, fast checkout experience for your audience.

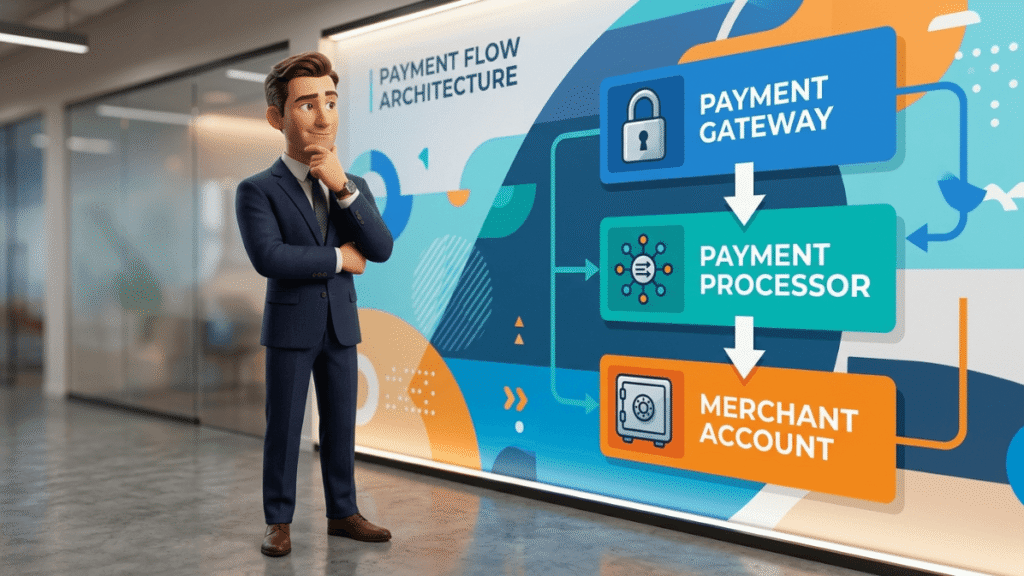

The Architecture of Payment Processing

Many digital store owners view payment acceptance as a single software tool.

In reality, learning how to receive credit card payments online relies on a multi-layered financial infrastructure.

Each layer serves a specific purpose to verify, authorize, and settle funds cleanly.

The Payment Gateway

This represents the digital perimeter of your checkout framework. It captures payment details.

It encrypts the primary account number. Finally, it acts as a virtual point-of-sale terminal. For an e-commerce store selling digital courses, this takes the form of an embedded checkout field on the web page.

The Payment Processor

This handles the heavy technical routing behind the scenes. It receives the encrypted data from the gateway.

Then, it transmits it directly to the card network. The processor communicates with the customer’s bank to verify funds.

It checks security parameters. It returns an approval or decline code to your sales platform.

The Merchant Account

Approved funds do not deposit into a standard checking account immediately. They route to a merchant account.

This is a commercial bank asset. It is specifically designated to handle card liabilities, settlement buffers, and transaction reversals. Once cleared, funds pass into your primary business checking account.

Structural Comparison of Account Options

Select your merchant presence to dictate your long-term processing expenses. It controls your contract flexibility and account stability.

Most companies looking at how to receive credit card payments must choose between a shared ecosystem approach or an independent commercial arrangement.

| Operational Vector | Shared Service Systems (Aggregators) | Dedicated Commercial Merchant Accounts |

| Account Ownership | Your business shares a massive, collective commercial pool with other entities. | Your business secures an individual, standalone merchant ID (MID). |

| Underwriting Standards | Instant, algorithmic approval with minimal up-front documentation. | Deep manual verification checking credit histories and industry risk. |

| Fee Architecture | Flat-rate structures combining all base costs into one fixed rate. | Interchange-plus structures splitting raw card network costs from profit markups. |

| Risk Environment | High susceptibility to automated account holds or processing freezes. | Exceptional stability because your specific risk was vetted up front. |

| Ideal Operational Scale | Low-volume environments processing under $20,000 monthly. | Enterprise setups processing over $25,000 monthly. |

Complete Framework for Receiving Credit Card Payments

Establishing your collection system requires precise execution. This prevents compliance penalties or onboarding delays.

This sequence breaks down the mandatory steps to transition from layout planning to live transaction capture.

Phase 1: Define Your Primary Sales Environment

Map out exactly how your customers buy from you. Your model might operate purely through a website checkout.

In that case, your setup requires a web-compatible digital gateway. Your workflow might require billing clients after services are rendered. Then, you need digital invoicing portals. In-person setups require mobile or fixed countertop hardware.

Phase 2: Select Your Commercial Account Model

Match your actual transaction volume against the core account choices. You might be validating a new business model with unpredictable sales.

Choose a flat-rate shared provider to avoid monthly maintenance fees. Your processing might consistently exceed $20,000 a month.

Apply for an independent merchant account to access lower wholesale rates.

Phase 3: Submit Business Records for Underwriting Verification

Provide your exact business documentation to your processor. You must supply your corporate Employer Identification Number (EIN).

Include your registered Articles of Organization. Provide verified business banking routing paths as well.

Merchant underwriters analyze these documents. They calculate your operational risk profile before activating your account.

Phase 4: Configure Technical Integrity and Software Connections

Embed your processing tools into your business operations. For online platforms, configure safe payment fields.

Use direct API keys or official integration modules. For physical point-of-sale setups, link your hardware terminals to local networks. Pair mobile card readers with your main management applications.

Phase 5: Verify Security and Achieve PCI Compliance Status

Complete your required Self-Assessment Questionnaire. This proves your network conforms to Payment Card Industry Data Security Standards. Verify your software settings.

It must never record or log raw account numbers on your local hard drives. Use secure tokenization methods to shield customer identities during checkout.

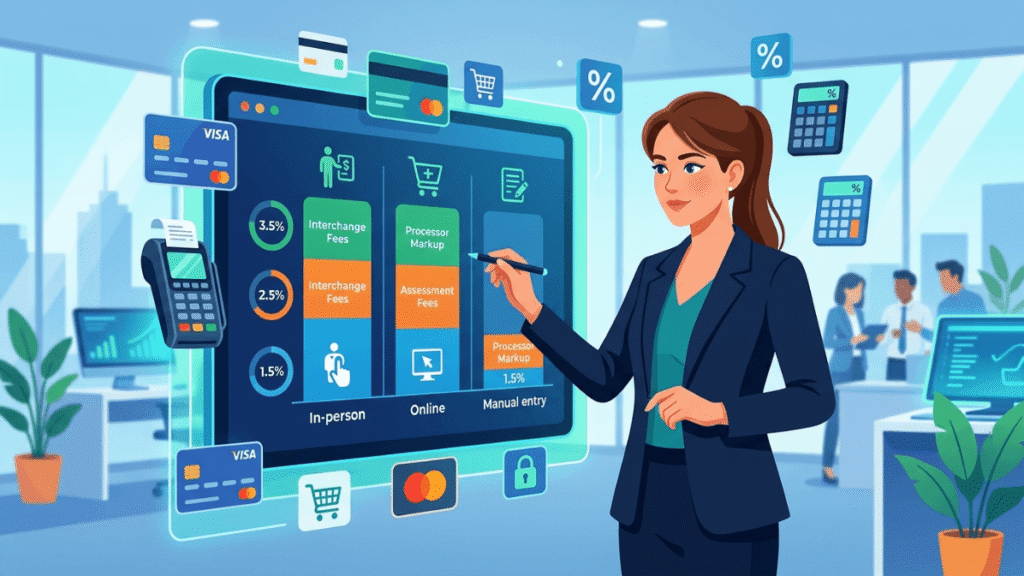

How to Analyze the True Costs of Interchange Fees

To manage your expenses efficiently, you must look closely at how processing bills are calculated. The total cost of every card swipe consists of three parts:

The direct cost to receive credit card payments typically ranges between 1.5% and 3.5% per transaction.

The exact rate depends on how you take the payment:

- In-Person Sales (Cards Swiped/Dipped/Tapped): Lowest cost, usually 1.5% to 2.5%.

- Online Sales & Digital Invoices: Higher risk, usually 2.5% to 3.5%.

- Manual Typing (Phone Orders): Highest risk, usually 3.5% or more.

The largest component is the interchange fee. It goes directly to the card-issuing bank. It covers funding risk and fraud protection.

Assessment fees are small, non-negotiable cuts. Networks like Visa or Mastercard take them to run their routing infrastructure.

The processor markup is the only fee you can negotiate. It represents the cut taken by your processing partner for managing your account.

Interchange rates fluctuate based on card types, merchant categories, and data submission levels.

A recent landmark Visa and Mastercard swipe fee settlement updated these rules.

It capped standard consumer credit card interchange rates at 1.25% for the next eight years.

This change offers meaningful relief. It gives more flexibility for your business trying to control checkout expenses.

| Card Network | Typical Base Interchange Range | Network Assessment Rate |

| Visa | 1.15% + $0.05 to 2.40% + $0.10 | 0.14% of overall volume |

| Mastercard | 1.15% + $0.05 to 2.50% + $0.10 | 0.1375% of overall volume |

| Discover | 1.40% + $0.05 to 2.40% + $0.10 | 0.13% of overall volume |

| American Express | 1.43% + $0.10 to 3.30% + $0.10 | 0.165% of overall volume |

Tactical Strategies to Reduce Expenses

Merchant expenses erode bottom-line profitability if left unmanaged. You can lower their effective transaction costs by applying these field-tested methods:

Transition Pricing Strategies Above Volume Benchmarks

Using a flat-rate processing model keeps things simple when starting. However, your monthly volume might pass $20,000.

At that point, flat-rate pricing becomes an expensive burden. Transitioning your organization to an interchange-plus framework allows you to pay true card network costs directly. This lets you bypass heavy corporate markups.

Optimize Virtual Shipments Using Comprehensive Data

Processing corporate B2B transactions or government orders requires deep data verification.

Submit detailed Level 2 and Level 3 transaction information. This includes sales tax tracking, customer accounting codes, and invoice specifics.

This data lowers your transaction risk tier. It qualifies your business for lower interchange rates, saving up to 1% per transaction.

Deploy Safe Digital Billing Links

Typing card numbers into a virtual terminal during phone orders is risky. It triggers maximum card-not-present rates.

Instead, generate an automated digital billing invoice link from your gateway. Text or email it directly to the customer’s phone. This allows the customer to authorize the transaction securely via an encrypted browser or mobile wallet. It lowers your overall risk profile.

My Client Solutions From the Field

As a remote freelancer, I fix broken payment setups for my clients. Many growing businesses lose money on transaction fees without realizing it. I audit their data to find these hidden leaks.

Below are four direct case studies. They show the exact processing problems I solved for my clients.

Save a Digital Brand $300 a Month

A digital services client used a basic flat-rate billing setup. Their monthly sales quickly scaled past $35,000.

This spike pushed their monthly processing bills over $1,000. I audited their account and switched them to an interchange-plus merchant plan. This single change cut their processing costs by $300 every month.

Stop Phone Order Penalty Fees

A retail client noticed massive extra fees on their monthly statements. I discovered their office staff typed credit card numbers manually during phone orders.

This manual typing triggered severe card-not-present penalty rates. I fixed this by setting up secure digital payment links sent via text. This move protected their margins and kept the checkout clean.

Block Expensive Chargeback Fraud

An equipment distributor lost a costly chargeback dispute. A customer claimed they never received their high-value package.

The client lacked a digital delivery signature linked to the transaction record, so the bank ruled against them.

I upgraded their gateway to require authenticated mobile wallet checkout for large orders. This step protects them from fraud liability.

Lower Billing Costs for a Service Business

A remote service client struggled with high overhead costs on phone orders.

I reviewed their dashboard and found staff manually keying in raw card numbers.

I resolved this issue by installing an automated invoicing system. Now, the system emails secure payment portals directly to buyers.

This quick adjustment saves the client hundreds of dollars every month.

Conclusion

Establishing a reliable payment solution changes everything for your business growth.

You will no longer waste time chasing unpaid invoices or dealing with manual collection errors.

Instead, your business gains a smooth revenue pipeline that operates quietly in the background.

Implementing these verified processing steps gives you total control over your overhead costs.

Your customers will enjoy a secure, fast checkout experience. Your daily business cash flow will remain steady and entirely predictable.

With your payment architecture securely in place, you can finally shift your complete focus back to scaling your business and serving your audience.

FAQ

What are the accurate cost percentages per transaction?

Comprehensive market reports from Nav small business financial tracking show clear industry averages.

Small businesses pay an effective rate between 1.5% and 3.5% per credit card transaction.

This comprehensive cost includes base network interchange rates. It contains system routing fees. It also includes the specific markup required by your merchant partner.

Why do digital card-not-present transactions carry higher costs?

You need to research how to receive credit card payments properly. Notice that physical card reads carry low rates.

Online sales, digital invoicing, or over-the-phone orders are different. They are classified as Card-Not-Present (CNP) transactions.

These channels carry a higher risk of fraudulent behavior. Therefore, card networks impose higher base interchange rates to balance that risk.

Can my business pass card processing costs directly to consumers?

Surcharging credit transactions is legal in most US states. However, it requires strict compliance with card network regulations.

Surcharges cannot exceed your actual processing cost. They also cannot exceed a hard ceiling of 3% to 4%.

Furthermore, surcharges can only apply to credit card purchases. Applying a surcharge to debit cards or prepaid cards is illegal. Clear signage must notify buyers at the point of sale.

How long does it take for funds to arrive in my primary checking account?

Standard transaction settlements usually take 2 to 3 business days to land in your account.

Some processing partners offer instant payouts for an extra fee. However, relying on standard settlement intervals protects your daily operational margins.

What specific documentation is required to clear merchant account underwriting?

You must provide a valid Employer Identification Number (EIN) issued by the IRS. Provide commercial banking routing paths.

Include a physical business address as well. Underwriters use these records to confirm your business is legitimate before approving processing access.

What steps should a business take if an account is suddenly frozen?

Immediately contact your processor’s risk department. Identify the specific trigger. Common reasons include a sudden sales spike or a high chargeback ratio.

Provide invoice records, tracking details, and fulfillment proof quickly to resolve the issue. This unlocks your processing path.

How does mobile wallet acceptance affect my checkout experience?

Accepting mobile wallets allows customers to confirm purchases instantly. They use biometric security on their devices.

This smooth process removes friction from your checkout flow. It lowers cart abandonment rates. It also keeps your transaction data secure.

What is the difference between a chargeback fee and a standard processing fee?

A processing fee is a regular cost deducted for routing a successful transaction. A chargeback fee is an extra penalty.

It ranges from $15 to $50. The network charges it when a customer officially disputes a charge through their credit card issuer.

Is it possible to accept credit card payments without a dedicated website?

Yes, you can receive payments by using virtual terminals or digital invoicing software.

These tools let you type in transaction details during phone orders. You can also email secure billing links directly to clients.

How do seasonal business shifts impact merchant account fees?

Some traditional commercial accounts charge fixed minimum monthly processing fees. They apply even when your sales volume drops.

Your business might have long dormant periods. Choosing a flat-rate processor ensures you only pay when you actually make a sale.

Why do international transactions incur extra costs?

Cross-border purchases require extra routing across different banking systems.

They also use currency translation frameworks. Processors typically add an extra 1% to 1.5% fee to handle these international compliance steps.

Can my business terminate a processing contract if rates increase?

You might use a month-to-month service provider. In that case, you can close your account at any time without penalty.

You might have an independent commercial contract instead. Review your agreement carefully to check for early termination fees or auto-renewal terms before changing partners.

Aliza Khatun is a Digital Marketing Professional and the founder of DigiGenHub. She has helped various businesses grow their online presence through real-world experience in marketing, branding, traffic growth, and business strategy.

Through DigiGenHub, she shows how to build and grow a business from the ground up using Website Setup, SEO, Branding, Paid Promotion, and smart digital tools.

She also highlights how AI can be used to its full potential to make content creation, automation, marketing, and business growth faster and smarter.

She believes that the right knowledge, modern technology, and the right tools can help any individual or business build a stronger online presence.