You open a store. Sales grow. Then one bad shipment, one customer claim, or one hacked checkout page wipes out months of profit in a single week. That is not a rare story. It happens to thousands of US online sellers every year.

Business insurance for online sellers is what stands between a rough month and a business-ending loss.

In 2026, platforms enforce it, courts expect it, and skipping it is one of the most expensive decisions a seller can make.

Today I’ll tell you exactly what coverage you need, what it costs, what platforms require, and how to set it up without overpaying.

The Hidden Risks Most Sellers Ignore

Selling online looks simple from the outside. But every order you ship carries layered risk. A product can injure someone.

A cargo container can sink. A hacker can drain your checkout data overnight. A platform can freeze your account with 30 days notice.

Most sellers focus on traffic and conversion. Risk sits quietly in the background until it does not.

The SBA’s business insurance guide puts it plainly: small businesses face the same liability exposure as large ones.

Court size does not shrink because your store does. One serious product claim can exceed your entire annual revenue.

Here is what makes online retail different from a physical store. Your operation runs across multiple systems at once.

Your inventory moves through several hands. Your payment data touches dozens of servers. Each connection point is a gap. Each gap is a potential claim.

Situations That Changed How I Cover My Clients

I manage e-commerce store operations remotely for several US sellers. I handle dashboards, supplier coordination, inventory tracking, and platform compliance daily.

These four situations are ones I worked through personally. Each one shaped the coverage I now prioritize for every client.

Situation 1: A Private Label Product Scorched a Kitchen

One of my clients sold imported kitchen accessories under their own brand name. A unit short-circuited inside a buyer’s home and scorched an expensive stone countertop.

The buyer’s attorney filed against my client’s business immediately. It did not matter that an overseas factory built the device.

My client’s name was printed on the box. That made them the responsible party in the claim.

I pulled their commercial liability policy the same day. It absorbed the full settlement cost.

Without that coverage, their business account would have been emptied in one case. This happens more often than sellers expect with private-label products.

Situation 2: Amazon’s 30-Day Compliance Deadline Hit Without Warning

I watched a client’s Amazon sales cross $10,000 in a single month. Less than 24 hours later, a compliance notification appeared in their dashboard.

Amazon gave exactly 30 days to upload a verified Certificate of Insurance. Miss the deadline and all listings freeze. Payouts stop. The account goes into suspension.

I reached a broker that afternoon. We had a qualifying policy and a valid certificate within days.

The account stayed open. Sellers who wait until the notification arrives often scramble too late. Get covered before you cross the threshold, not after.

Situation 3: A Holiday Cargo Shipment Was Destroyed at Sea

I coordinate freight and supplier communication for an import client. Last peak season, their largest holiday stock shipment hit severe ocean weather.

Several pallets were crushed inside the container. Water entered and ruined the rest. The freight carrier cited standard exemption clauses and denied the full claim.

My client kept an active inland marine transit policy. It covered the true replacement cost of the inventory.

We sourced backup stock immediately. They did not miss the holiday window. Without that policy, the loss would have been absorbed entirely out of cash flow.

Situation 4: A Warehouse Endorsement Gap Cost 40 Percent of a Claim

A client stored their full inventory in one regional warehouse. A sprinkler system malfunction caused water damage across two product lines.

Their commercial property policy paid out, but the coverage cap was set during a slower quarter. Inventory had doubled since then.

The payout covered roughly 60 percent of the actual replacement cost. The remaining 40 percent came out of working capital.

That gap hurt their cash position for two months. We added a Peak Season Endorsement immediately.

It automatically raises coverage limits during high-volume periods. Set your property limits based on your peak inventory value, not your average.

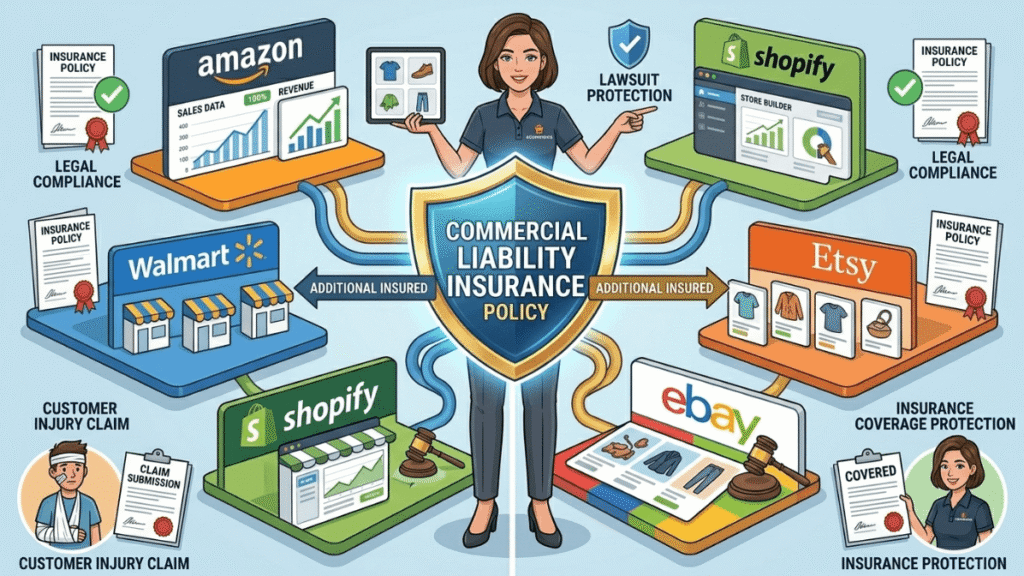

What Every Major Platform Requires in 2026

Platforms do not remind you about insurance out of goodwill. They enforce it to protect their own legal position.

Check the Amazon seller insurance requirements directly in Seller Central. So you know exactly what your certificate must show.

| Platform | Coverage Required | Sales Trigger | Key Rule |

| Amazon | $1M per occurrence general liability | $10,000/month gross proceeds | Amazon must be named as additional insured; max $10K deductible |

| Walmart Marketplace | $2M aggregate minimum | $100,000 in 12-month GMV | Stricter limits than Amazon |

| Shopify | No platform requirement | None | Legal exposure identical to Amazon sellers |

| Etsy | No platform requirement | None | Legal exposure identical to Amazon sellers |

| eBay | No platform requirement | None | Legal exposure identical to Amazon sellers |

Shopify not requiring coverage does not reduce your risk. A product that injures a buyer creates the same lawsuit whether it sold on Amazon or your own Shopify store. The platform requirement protects the platform. Your policy protects you.

One policy covers all of them. You add each marketplace as an Additional Insured on your certificate.

That single certificate satisfies Amazon, Walmart, Etsy, Shopify, and any other channel at the same time.

The Four Policies Every Online Seller Needs

To protect your bottom line, you cannot rely on luck. One bad accident or lawsuit can close your shop overnight.

These four essential insurance policies form your ultimate safety net. They make sure a single crisis does not end your business.

1. General and Product Liability Insurance

This is the core policy. It covers legal defense costs, attorney fees, and settlement payouts when a buyer claims your product caused physical injury or property damage. It also covers advertising injury claims.

The critical fact most sellers miss: you do not have to manufacture a product to be held liable for it.

US strict liability law puts every entity in the supply chain on the hook. If you import it, white-label it, or private-label it and sell it under your store name, you are treated as the manufacturer in court.

Set your liability limits based on worst-case injury severity, not your current monthly revenue.

2. Cyber Liability Insurance

This is the policy most online sellers skip and the one that causes the most financial shock when something goes wrong.

The FBI’s 2025 Internet Crime Report recorded $20.877 billion in US cybercrime losses, a 26 percent jump from 2024 and the first time the figure crossed $20 billion.

That number only reflects reported incidents. The actual total is estimated to be several times higher.

For US businesses specifically, IBM’s Cost of a Data Breach 2025 found the average breach cost hit $10.22 million per incident. An all-time high and more than twice the global average.

Even a small breach involving customer email addresses and shipping data can trigger notification requirements, regulatory fines, and customer lawsuits.

Your checkout page, customer database, and stored payment records are active targets.

A breach halts checkout instantly. It can freeze platform accounts pending review. It burns customer trust in ways that are hard to recover from.

Cyber liability insurance covers data recovery costs, forensic investigation fees, customer notification expenses, and regulatory fines. Get it before you need it. Underwriting requirements tighten every year.

3. Inland Marine and Transit Insurance

Standard commercial property coverage only applies to inventory at a fixed, named address. Your inventory is constantly moving.

It sits at freight docks, travels by truck between fulfillment centers, and spends weeks at sea inside cargo containers.

Inland marine coverage travels with your goods. It protects stock in transit across land.

Ocean cargo coverage handles international shipments. If a carrier claims exemption during a weather event or accident, your transit policy covers the actual replacement value of the lost goods. Without it, you absorb that cost entirely.

4. Commercial Property Insurance

This protects inventory sitting in your warehouse or storage facility. Set limits based on full replacement cost at today’s prices, not original purchase price.

If you store stock at more than one location, each address must be covered. A single-address policy leaves every other location unprotected.

Add a Peak Season Endorsement if your inventory value rises significantly during Q4 or other peak periods.

Standard flat caps frequently leave seasonal sellers underinsured at exactly the wrong time.

2026 Premium Benchmarks: What Each Policy Costs

These are national US averages. Your actual quote depends on product category, annual revenue, fulfillment setup, and claims history. Use these numbers to build your coverage budget.

| Policy Type | Avg Monthly Premium | Main Pricing Factor |

| General and Product Liability | $137 | Product risk level, material types, regional court trends |

| Cyber Liability | $138 | Monthly transaction volume, customer data stored |

| Inland Marine and Transit | $31 | Shipping distance, cargo value, freight method |

| Commercial Property | $262 | Facility location, regional weather risk, total stock value |

| Business Owners Policy (BOP) | $33 and up | Bundles GL and property; good starting point for smaller stores |

High-risk categories like children’s products, health supplements, electronics, and power tools carry higher premiums.

Apparel, home decor, and books sit at the lower end. Your product category affects your rate more than your store size does.

Top Insurance Providers for Online Sellers in 2026

Several providers now specialize in e-commerce coverage with instant certificates and marketplace-compliant formats. Here is how the main options compare.

| Provider | Best Fit | GL Starting Cost | Key Strength |

| NEXT Insurance | Amazon FBA, multi-platform sellers | From $13/month | Instant COI in Amazon-approved format; 24/7 certificate access |

| The Hartford | Product businesses needing bundled coverage | BOP from $33/month | A+ AM Best rating; strong claims handling |

| Thimble | Etsy sellers, small and seasonal stores | Flexible by month or project | Pay only for the time you need coverage |

| Insurance Canopy | Amazon sellers needing fast compliance | Varies by product type | Certificate delivered within 24 hours of approval |

| Assureful | Seasonal brands, DTC stores | Pay-as-you-sell pricing | Premiums scale with actual store revenue, not estimates |

All five allow a single policy to cover multiple sales channels. Name each platform as an Additional Insured on your certificate. One policy. One certificate. Every platform satisfied.

How to Set Up Your Coverage in Four Steps

Follow this sequence. It avoids overpaying and closes the most common coverage gaps.

Step 1: Calculate your true inventory replacement value

Pull your latest supplier invoices. Add up what it costs to replace your entire stock at today’s prices. That number, not last year’s figure, sets your commercial property limit. Undervaluing this is the single most common mistake sellers make.

Step 2: Read your platform compliance clauses directly

Log into every marketplace dashboard you sell on. Find the exact insurance language in their seller agreement. Confirm your policy matches their per-occurrence limit, aggregate limit, deductible cap, and additional insured requirement. Do not rely on summaries. Read the original clause.

Step 3: Compile your supplier documentation

Gather material safety data sheets, product test certifications, and quality agreements from your factories.

Presenting these to underwriters shows documented risk management. It often produces a lower quoted premium. Suppliers with no documentation are a red flag to insurers and can raise your rate.

Step 4: Get at least two quotes, then download your certificate

Submit your business details to two or three e-commerce insurance brokers. Compare coverage structure, exclusions, and deductibles, not just monthly price.

Choose the plan that fits your fulfillment model. Download your Certificate of Insurance. Upload it to every marketplace that requires it before your next sales milestone hits.

When to Update Your Policy

Coverage that fits today may leave gaps in six months. Watch for these four triggers and update your policy before the gap becomes a claim.

You add a new product category

Electronics, skincare, children’s toys, and supplements carry different liability profiles than your existing products. Update your policy before you ship the first unit of anything new.

You launch on a new platform

Each marketplace has its own insurance requirements. Walmart’s thresholds and minimums differ from Amazon’s. Check the compliance language before your first listing goes live.

You split inventory across multiple warehouses

Each storage location needs its own property coverage address. A policy tied to one warehouse leaves all others unprotected.

Your monthly transaction volume rises significantly

More orders mean more customer data. More data means higher cyber exposure. Your cyber liability limits should grow alongside your order volume.

Three Proven Ways to Cut Your Premium Costs

You can reduce your monthly insurance costs without reducing your coverage.

These three habits create documented risk reduction that insurers price into your renewal quote.

Enforce multi-factor authentication across all accounts

Require it on every staff email, store backend, supplier portal, and payment system.

Tight access control is the single most effective cyber risk reducer. Insurers recognize it and price it into your cyber premium at renewal.

Add hold-harmless clauses to your supplier contracts

Every factory agreement should include clear language stating that the manufacturer bears financial responsibility for production defects.

Documented shared liability lowers your product liability premium. No documentation means you absorb the full risk alone.

Distribute inventory across multiple fulfillment locations

One warehouse holds one fire risk. Split stock across two or three regional centers and no single event can wipe out your entire inventory.

That reduced maximum loss is reflected in your commercial property premium.

The Verizon 2025 Data Breach Report Numbers Every Seller Should Know

The 2025 Verizon DBIR found ransomware in 44 percent of all confirmed breaches, up from 32 percent the year before.

Small and mid-sized businesses experienced four times more confirmed breaches than large enterprises.

Attackers are not skipping small stores. They are targeting them more specifically because defenses tend to be weaker.

These numbers matter for sellers specifically. A ransomware attack on your store backend locks you out of your inventory system, order management, and payment processing simultaneously.

Every hour offline during a peak sales period is permanent lost revenue. Cyber liability insurance covers the forensic response, the system restoration, and the regulatory notification costs that follow.

Final Checklist Before You Buy

Go through these before you submit your first application.

- Know your total inventory replacement value at today’s prices

- Know the exact compliance requirements for every platform you sell on

- Have your supplier quality documentation organized and ready

- Know your highest-risk product category and its liability profile

- Decide whether you need a standalone BOP or separate individual policies

- Confirm each marketplace will be named as Additional Insured

- Set a calendar reminder to review limits at every major inventory or sales milestone

Closing Thoughts

Business insurance for online sellers does not prevent bad things from happening. It prevents bad things from ending your business when they do happen.

Platforms will not absorb your claim. Suppliers will not cover your legal fees. Your personal insurance will deny your commercial losses. A properly structured commercial policy is the only thing that absorbs the financial shock so your store keeps running.

The cost of coverage is predictable. The cost of a single uninsured claim is not. Get your coverage in place before your next sales milestone, not after the notification lands in your dashboard.

Business insurance for online sellers is one decision that protects every other decision you make.

FAQ

Does my homeowners or renters insurance cover my online store?

No. Personal property policies explicitly exclude commercial business activity. A $30,000 inventory fire in your home garage gets denied. You need a dedicated commercial policy regardless of where you store your stock.

Am I legally responsible for products I did not make?

Yes. US strict liability law holds every seller in the supply chain responsible. Importing, private-labeling, or white-labeling a product puts you in the same legal position as the manufacturer. Your store name on the box is enough to be named in a lawsuit.

Can a single policy cover Amazon, Shopify, and Etsy at once?

Yes. One commercial policy covers your entire business operation. Name each platform as an Additional Insured on your certificate. You do not need separate policies per channel.

Does insurance cover payment fraud or chargebacks?

No. Payment processors handle chargebacks. Insurance excludes billing disputes entirely. Use real-time fraud detection software at your checkout to block suspicious orders before they ship.

What if my primary supplier goes bankrupt?

Insurance does not cover lost sales from a supplier closing. Only physical damage to goods triggers a payout. Diversify your supply chain across at least two independent manufacturers to reduce this exposure.

Does weather-related shipping delay trigger a claim?

No. Delays alone are not covered. Coverage activates only if weather physically destroys your inventory in transit. Keep regional backup stock during peak season to absorb delay risk without insurance involvement.

Are my gift card balances protected in a data breach?

Standard policies exclude digital gift card balances because they represent cash value, not data. Add a Commercial Crime endorsement to cover stolen virtual fund balances specifically.

What if a software glitch deletes all my store data?

Standard cyber policies cover external attacks. Internal software errors need an Errors and Omissions endorsement. It covers financial recovery from internal coding mistakes and system failures.

Aliza Khatun is a Digital Marketing Professional and the founder of DigiGenHub. She has helped various businesses grow their online presence through real-world experience in marketing, branding, traffic growth, and business strategy.

Through DigiGenHub, she shows how to build and grow a business from the ground up using Website Setup, SEO, Branding, Paid Promotion, and smart digital tools.

She also highlights how AI can be used to its full potential to make content creation, automation, marketing, and business growth faster and smarter.

She believes that the right knowledge, modern technology, and the right tools can help any individual or business build a stronger online presence.