You need capital. But you do not want to lose equity. You also do not want a bank loan that demands perfect credit and two years of tax returns. Sound familiar?

That is why revenue-based financing is popular now. It fills the gap between where bank lending stops and where equity deals begin.

It gives you cash now. You pay it back from your future sales. No fixed schedule. No equity loss.

What Is Revenue-Based Financing?

Revenue-based financing (RBF) is a funding model. Here, you can receive a lump sum of capital and repay it as a fixed percentage of your monthly gross revenue. Payments rise when your sales are strong. They drop when sales slow down.

You repay until you hit a preset total, usually 1.3x to 1.7x the original amount. That multiplier is called the repayment cap.

For example: You get $100,000 at a 1.5x cap. You repay $150,000 total. If your revenue is high one month, you pay more. If it drops, you pay less. No penalties either way.

This is very different from a bank loan with a fixed monthly bill or venture capital that takes a slice of your company.

How Revenue-Based Financing Works, Step by Step

Let’s learn the typical flow:

- You apply to an RBF provider with your revenue records (bank statements, Stripe, QuickBooks, etc.)

- The provider reviews 3 to 12 months of revenue data

- They offer you capital based on your monthly recurring revenue (MRR) or annual recurring revenue (ARR)

- You agree on a repayment percentage (typically 2% to 10% of monthly gross revenue) and a cap (1.3x to 1.7x)

- Funds hit your account in 24 to 72 hours for most fintech providers

- Each month, the agreed percentage is automatically pulled from your revenue

- Once the cap is hit, the agreement ends

No collateral. No equity. No board seat. No personal guarantee in most cases.

The Recent Market: Why This Is Growing So Fast

The numbers tell the story clearly.

Revenue-Based Financing Market Size (2023–2035)

| Year | Market Size (USD) | Source |

| 2023 | $6.4 billion | Allied Market Research |

| 2024 | $12.9 billion | Verified Market Reports |

| 2026 | $5.38–$15.86 billion (range by methodology) | GlobalGrowthInsights / Research and Markets |

| 2033 | $35.7 billion (conservative) | Verified Market Reports |

| 2033 | $178.3 billion (aggressive) | Allied Market Research |

| 2035 | $16.5 billion | GlobalGrowthInsights |

Sources: Allied Market Research | Verified Market Reports | GlobalGrowthInsights

The wide range in projections exists because different firms define the RBF market differently. But every single one points to explosive growth.

Why the surge?

- 68% of startups now prefer non-dilutive capital over equity deals

- 63% of digital businesses favor repayment tied to revenue performance

- 64% of funded businesses report better cash-flow management after adopting RBF

- Traditional bank approval rates for small businesses sit below 50%

- Venture capital has grown more selective and harder to access post-2022

North America leads with roughly 60% of global RBF volume. The US and Canada dominate due to large tech startup ecosystems and a mature alternative lending market.

Who Qualifies for Revenue-Based Financing?

RBF is not for every business. It works best for companies with:

- At least $10,000 to $50,000 in monthly recurring revenue (varies by provider)

- 6 to 12 months of consistent revenue history

- Revenue that comes in regularly (subscriptions, recurring contracts, repeat e-commerce sales)

- Healthy gross margins (usually 40% or more preferred)

- No requirement for physical collateral

Best fits by business type:

- SaaS and software companies

- E-commerce stores with repeat buyers

- Digital agencies with retainer clients

- D2C subscription brands

- App-based businesses

Not a great fit for:

- Pre-revenue startups

- Businesses with highly irregular or seasonal-only revenue

- Businesses with very thin margins (under 20-25%)

- Retail stores or restaurants with mostly cash-based, unpredictable revenue

What Does Revenue-Based Financing Cost?

This is the part most articles skip over. Let us be direct.

RBF uses a factor rate instead of an interest rate. A factor rate of 1.3 means you pay back $1.30 for every $1 borrowed.

The factor rate typically ranges from 1.1 to 2.5 depending on the provider and your risk profile.

Cost Example:

| Loan Amount | Factor Rate | Total Repayment | Extra Cost |

| $50,000 | 1.3x | $65,000 | $15,000 |

| $100,000 | 1.5x | $150,000 | $50,000 |

| $200,000 | 1.7x | $340,000 | $140,000 |

The effective APR can range from 20% to 40%+. If your revenue is strong and you repay quickly, your effective APR becomes higher because you reach the repayment cap sooner.

If revenue is slower, repayments are spread over a longer period. That’s why revenue-based financing is usually more expensive than a bank loan.

However, it can still be cheaper than giving up equity if your company grows 10x.

Rakib, my friend, funded a content agency through RBF once. He and his team took $80,000 at a 1.4x cap. They repaid $112,000 over 11 months. Their effective cost was around $32,000.

That same period, their revenue grew from $28k to $61k monthly. No equity was touched. That $32k cost felt very reasonable for the growth we funded.

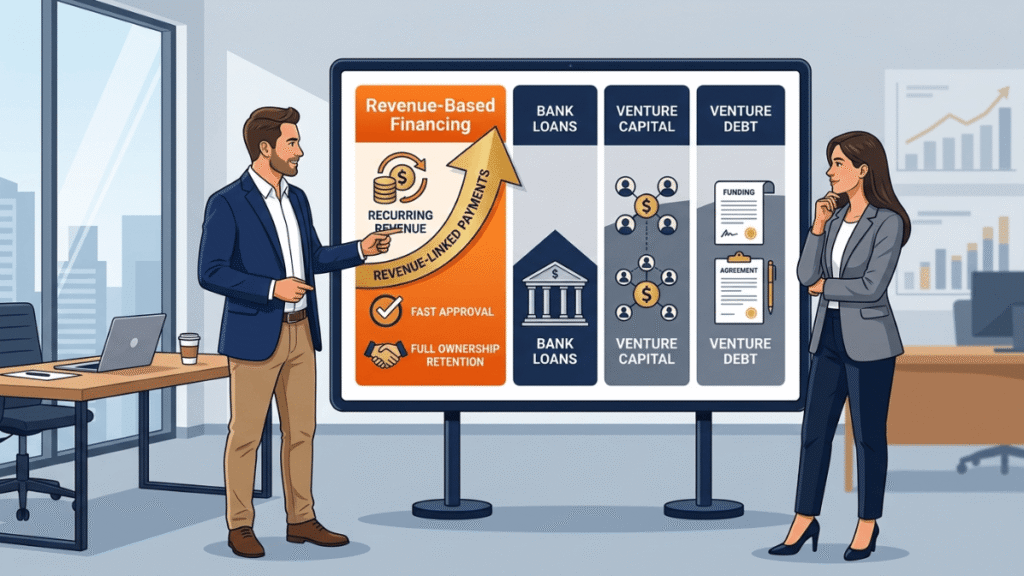

Revenue-Based Financing vs Other Funding Options

This is where most founders get confused. Here is a direct comparison.

Funding Options Compared (2026)

| Factor | RBF | Bank Loan | Venture Capital | Venture Debt |

| Equity given up | None | None | Yes (significant) | Sometimes (warrants) |

| Collateral required | No | Often yes | No | Sometimes |

| Approval speed | 24–72 hours | Weeks to months | 3–12 months | Weeks |

| Repayment flexibility | Adjusts with revenue | Fixed monthly | No fixed repayment | Fixed monthly |

| Revenue requirement | Yes (recurring preferred) | Yes (2+ years) | No (but growth potential needed) | Yes (VC-backed usually) |

| Cost | 1.1x–2.5x cap | 6–15% APR | 20–40% equity + future dilution | 8–14% APR + warrants |

| Suitable for | SaaS, e-commerce, subscription | Established profitable businesses | High-growth, high-burn startups | VC-backed post-Series A |

| Board control lost | No | No | Often yes | Rarely |

Sources: Crestmont Capital | Flow Capital | Float Finance

The key decision is simple. If you have recurring revenue and need growth capital, RBF can be a good option.

It lets you raise money without giving up equity or signing personal guarantees.

If you need a large amount of funding, such as $5 million or more, and already have venture backing, venture debt is usually the cheaper choice.

If your business has traditional collateral and generates steady profits, a bank loan will typically cost less.

Pros and Cons of Revenue-Based Financing

Pros:

- No equity dilution. You keep 100% of your company

- Payments flex with revenue. Slow month? Pay less. Strong month? Pay more

- Fast funding. Most fintech RBF providers fund in 24 to 72 hours

- No collateral or personal guarantee typically required

- No board seats, no investor oversight, no term sheets

- Works for businesses that do not qualify for traditional bank financing

- No interest accumulation. You know the total repayment from day one

Cons:

- Higher cost than bank loans. Factor rates of 1.3x to 1.7x add up

- Limited to revenue-generating businesses. Pre-revenue startups cannot access it

- Smaller amounts than venture debt or equity rounds (most deals range from $10k to $5M)

- Some providers pull payments daily, which can feel tight on cash flow

- If revenue grows very fast, effective APR is high (you repay the cap quickly)

A Personal Lesson: When RBF Saved a SaaS Company from Dilution

A friend of mine runs a B2B SaaS platform with $180k monthly recurring revenue.

In early 2025, he needed $250,000 to hire two engineers and ramp up paid ads. Two VC firms offered term sheets.

But both asked for 18% equity at an $1.4M valuation. He felt that was deeply undervalued.

He went with RBF instead. Got $250k at a 1.45x cap. Repaid $362,500 over about 14 months.

The cost was $112,500. By the time he finished paying, his MRR had jumped to $310k and his valuation had grown to over $4 million.

If he had taken the VC deal, those investors would now own 18% of a $4M company, worth $720k.

He paid $112k for the same outcome. That math is why founders are choosing RBF over VC more often than ever before.

Top RBF Providers: A Tool Comparison for 2026

Different providers serve different business types. Here is a clear overview.

Revenue-Based Financing Providers Compared

| Provider | Best For | Funding Range | Approval Time | Repayment % | Notable Feature |

| Lighter Capital | SaaS, tech startups | $50k–$3M | 1–2 weeks | 2–8% of monthly revenue | Long track record in SaaS |

| Clearco | E-commerce, marketing | $10k–$10M | 24–48 hours | Flexible, revenue-linked | Marketing capital focus |

| Capchase | SaaS ARR monetization | $10k–$12M | 24–48 hours | Tied to ARR/MRR | Non-dilutive SaaS focus |

| Pipe | Subscription revenue | $50k–$10M | Days | Based on contracted ARR | Trades recurring revenue |

| Founderpath | SaaS bootstrapped | $1k–$10M | Fast | 1–12% | No equity, bootstrapper-friendly |

| Decathlon Capital | Growth-stage companies | $1M–$20M | 2–4 weeks | Variable | Larger deal specialist |

Note: Terms change frequently. Always verify directly with providers before applying.

I personally tested the application process on two of these platforms while running a client project. Both were surprisingly smooth.

The data connection (Stripe, QuickBooks) did the heavy lifting. One approval took under 36 hours.

The Remittance Rate: The Number That Changes Everything

The remittance rate is the percentage of monthly revenue you give up for repayment. This is the most important number in any RBF deal.

Typical remittance rates in 2026:

- SaaS businesses: 2% to 5% (lower because ARR is predictable and providers take less risk)

- E-commerce businesses: 7% to 15% (higher because revenue can be less predictable)

- Overall median: 5% to 7%

- About 78% of deals include a minimum monthly payment floor

If your monthly revenue is $100,000 and your remittance rate is 6%, you pay $6,000 that month toward your cap.

If next month revenue drops to $60,000, you pay $3,600. This automatic adjustment is the core benefit over a fixed-payment loan.

How to Apply: What You Need Ready

Getting RBF approval is far less painful than a bank loan. But preparation still matters.

Documents and data providers typically require:

- 6 to 12 months of bank statements

- Access to your payment processor (Stripe, PayPal, Shopify)

- Accounting software access (QuickBooks, Xero) in many cases

- 3 to 6 months of revenue data showing consistent monthly income

- Basic business information (entity type, time in business, industry)

Tips to improve your offer:

- Keep your revenue consistent. Providers like stability

- Show growth, not just flat revenue

- Higher gross margins usually mean better rates

- Having multiple revenue streams helps

- Avoid applying right after a bad revenue month

Most applications take 30 to 60 minutes. Decisions come in 24 to 72 hours for most fintech providers.

A Pattern I Keep Seeing with Seasonal Businesses

One of the trickier situations is seasonal revenue. Say you run an outdoor equipment e-commerce store. Revenue is $200k in summer, $20k in winter.

A fixed bank loan payment of $15,000 per month would crush you in February.

RBF with a 7% remittance rate means you pay $14,000 in summer months and only $1,400 in winter. Same deal, completely different cash flow pressure.

This is one of the clearest wins for revenue-based financing. It breathes with your business instead of strangling it.

Red Flags to Watch in Any RBF Deal

Not all providers are equal. Watch for these warning signs:

- Factor rates above 2x (that is very expensive; shop around)

- Daily payment pulls without your consent

- Prepayment penalties (you should be able to pay off early without extra cost)

- Confusing or buried terms around the remittance rate

- Providers who do not disclose the effective APR when asked

- Deals that require equity warrants (that is venture debt, not true RBF)

- Very short repayment windows with very high remittance rates

Always ask: what is my total repayment? What is my monthly remittance rate? Can I pay early? Is there a minimum monthly payment?

RBF vs Merchant Cash Advance: Do Not Confuse Them

Many people mix up revenue-based financing and merchant cash advances (MCAs). They are different.

| Feature | RBF | Merchant Cash Advance |

| Based on | Monthly recurring revenue | Daily credit card sales |

| Payment collection | Monthly (usually) | Daily deduction from sales |

| Typical cost | 1.1x to 2.5x | 1.2x to 1.5x (but often effectively higher) |

| Regulation | Growing regulatory oversight | Less regulated |

| Best for | SaaS, subscriptions, e-commerce | Retail, restaurants with card swipes |

| Transparency | Generally higher | Often lower |

MCAs pull payments daily, sometimes every business day. That daily drain can hit cash flow hard.

RBF is almost always monthly and tied to total gross revenue, not card transactions alone.

What Is Happening With RBF in 2026 Specifically?

Three shifts stand out this year:

1. AI-powered underwriting is faster than ever.

About 66% of RBF platforms now use automated underwriting. This means decisions that used to take two weeks now take hours. Your Stripe data, QuickBooks export, and bank connection do the work.

2. Larger deal sizes are available.

In 2023, most RBF deals topped out around $1M to $2M. In 2026, several providers now offer up to $10M to $12M, making RBF viable for mid-size companies that previously had to go to venture debt.

3. SaaS-specific structures are maturing.

Providers now build deals directly around ARR multiples. A company with $2M ARR might access $400k to $600k immediately. This removes the need to justify revenue month by month. Annual recurring revenue becomes collateral.

Final Thought

Revenue-based financing is not perfect for every business. But for SaaS companies, subscription brands, and e-commerce stores with consistent revenue, it solves a real problem.

You get growth capital fast. You keep your equity. You repay at the pace your business can handle.

The market has matured fast. Approval times are down. Deal sizes are up. Underwriting is smarter.

If you have recurring revenue and have been wondering whether revenue-based financing fits your situation, the answer is probably yes.

The next step is to pull three months of revenue data and start a conversation with two or three providers to compare offers.

FAQ

How much can I get with revenue-based financing?

Most providers offer between 1x and 3x your monthly recurring revenue, or 15% to 30% of your ARR. On a $50k MRR business, you might access $50k to $150k.

Does RBF affect my credit score?

Most RBF providers do a soft credit pull only during underwriting. Repayment activity is generally not reported to personal credit bureaus. However, defaulting can have consequences depending on the agreement.

Can I get RBF if my business is only 6 months old?

Some providers fund businesses as young as 6 months if revenue is consistent. Most prefer 12 months. The key is revenue stability, not age alone.

What happens if my revenue drops to zero?

Technically, a zero revenue month means zero payment due (since the remittance is a percentage). However, most deals have a minimum monthly payment clause. Check your contract carefully before signing.

Is revenue-based financing available outside the US?

Yes. The UK, Canada, Australia, and parts of Europe have active RBF providers. Asia-Pacific is the fastest-growing region for RBF adoption in 2026.

Can I use RBF alongside a bank loan?

Yes, in many cases. Some businesses use a bank line of credit for operational costs and RBF for growth initiatives like marketing or hiring. Check if your bank loan has covenants that restrict additional financing.

What is an RBF cap and why does it matter?

The cap is the total amount you repay expressed as a multiple of what you borrowed. A 1.5x cap on $100k means you repay $150k total, regardless of how long it takes. It protects you from open-ended cost escalation.

How does RBF treat early repayment?

In most RBF deals, paying more than your remittance percentage in any given month simply shortens the repayment period. There are usually no prepayment penalties. Confirm this before signing.

Is RBF right for a bootstrapped startup?

Often yes. Bootstrapped founders who want to stay independent love RBF because it provides growth capital without involving outside equity holders. Providers like Founderpath and Lighter Capital specifically serve bootstrapped SaaS founders.

How is RBF taxed?

RBF repayments are generally treated as debt repayment, not income. The cost above the principal (the cap minus the original amount) is typically deductible as a financing expense. Always confirm with your accountant based on your jurisdiction.

Aliza Khatun is a Digital Marketing Professional and the founder of DigiGenHub. She has helped various businesses grow their online presence through real-world experience in marketing, branding, traffic growth, and business strategy.

Through DigiGenHub, she shows how to build and grow a business from the ground up using Website Setup, SEO, Branding, Paid Promotion, and smart digital tools.

She also highlights how AI can be used to its full potential to make content creation, automation, marketing, and business growth faster and smarter.

She believes that the right knowledge, modern technology, and the right tools can help any individual or business build a stronger online presence.