A fulfillment center’s conveyor belt jams two days before Black Friday. A content creator’s camera rig dies the night before a product launch video.

An online bakery’s commercial mixer breaks down with a shipping deadline looming.

These moments push business owners straight into one search: equipment financing for small businesses.

What Equipment Financing for Small Businesses Means

Equipment financing pays for the tools a business runs on. Forklifts. Packaging machines. Servers. Cameras. Studio lights. Kitchen gear for a delivery-only kitchen. 3D printers for an online shop. If it has a price tag and gets used daily, it qualifies.

The equipment itself backs the loan. Miss a payment, and the lender takes the equipment back. Not your house. Not your savings.

That lowers the risk for lenders. Federal Reserve survey data shows it: approval rates for equipment-backed loans beat approval rates for unsecured business loans.

Print-on-demand sellers hit this pattern often. One owner, running a shop on Etsy and Shopify, needed a $38,000 direct-to-garment printer to keep up with orders.

A bank turned him down for a general loan. Thin collateral, they said. An equipment lender approved him in four days. The printer backed the deal, so the risk dropped.

That’s the gap between a no and a yes. Collateral closes it. Credit alone doesn’t.

How Equipment Financing Works

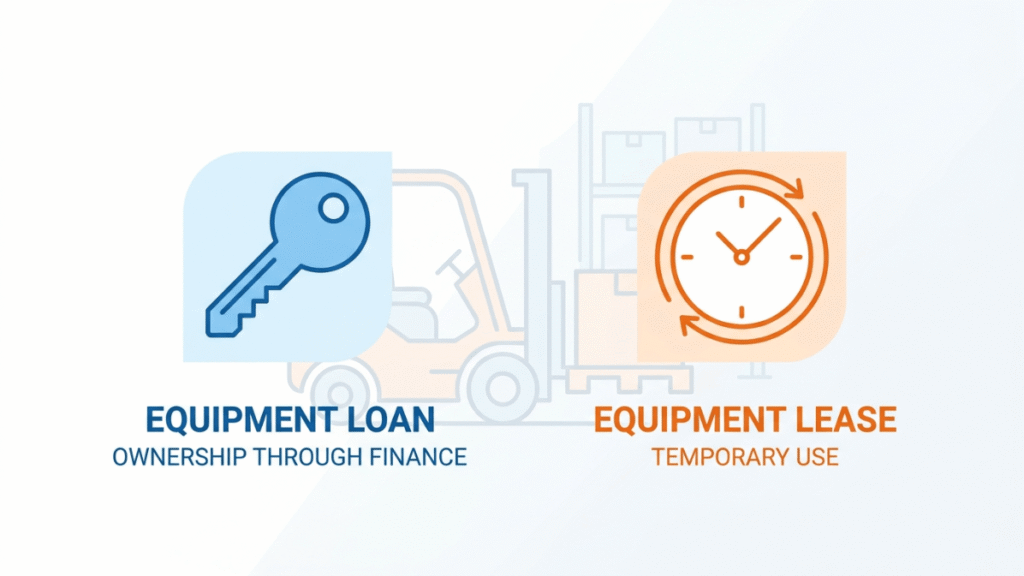

Two main paths exist: a loan or a lease.

With an equipment loan, you borrow money, buy the equipment, and own it once you pay off the balance. The lender holds a lien on the asset until then.

With an equipment lease, you pay to use the equipment for a set term. At the end, you return it, renew it, or buy it at a set price.

Leasing often needs less money down and keeps monthly payments lower, which helps cash flow during slow seasons.

An e-commerce fulfillment business I know leased her warehouse forklifts for years to upgrade gear every two seasons.

She switched to a loan once her order volume stabilized, since the forklifts held resale value better than she expected. That switch cut her yearly equipment cost by close to 18%.

Most owners pick a loan when they plan to keep the equipment for years. They pick a lease when the gear loses value fast, like cameras, computers, or diagnostic scanners, or when they want to upgrade every few seasons.

Types of Equipment Financing for Small Businesses in 2026

Five main paths cover almost every situation:

| Financing Type | Best For | Typical Term | Down Payment |

| Equipment loan (bank or credit union) | Owners with solid credit, keeping the equipment long-term | 2 to 7 years | 10% to 20% |

| Equipment lease | Fast-depreciating gear, frequent upgrades | 1 to 5 years | Often $0 |

| SBA 7(a) loan | Larger purchases bundled with other business needs | Up to 10 years for equipment | 10% |

| SBA 504 loan | Major fixed assets, heavy machinery | 10, 20, or 25 years | 10% |

| Online or alternative lender | Newer businesses, fast funding needs | 1 to 5 years | Often $0 |

Each path fits a different stage of business. A five-year-old shop with clean books usually qualifies for a bank loan at the lowest cost.

A business open eight months with steady monthly revenue often turns to a lender instead, even though the rate runs higher.

Equipment Financing Rates in 2026

Rates held mostly steady through early 2026 after the Federal Reserve paused rate cuts. The prime rate sat at 6.75% through the first half of the year.

Here’s what that means for actual borrowing costs:

| Financing Source | 2026 Rate Range |

| SBA 7(a) loan | 9.75% to 14.75% (capped by SBA rules) |

| SBA 504 loan | 5% to 7% (fixed) |

| Bank equipment loan | 7% to 12% |

| Credit union equipment loan | 6% to 10% |

| Lender | 12% to 30% |

| Equipment lease | Often equal to 8% to 16% APR |

The SBA sets maximum rate caps for 7(a) loans based on loan size and the prime rate. Lenders can charge less than the cap, but never more.

An online furniture retailer needed a $90,000 packaging and palletizing system for her warehouse last spring.

A bank quoted 8.5%. A lender quoted 22%. She took the bank loan and waited five extra weeks for funding. That wait saved her over $30,000 in interest across the loan term.

Section 179: The Tax Move Most Owners Miss

Equipment financing for small businesses pairs well with a tax rule called Section 179.

It lets you deduct the full cost of qualifying equipment in the year you place it in service, instead of spreading the deduction across many years.

For 2026, the numbers look like this, confirmed in IRS Publication 946:

- Maximum deduction: $2,560,000

- Phase-out starts at: $4,090,000 in total equipment purchases

- Fully phased out at: $6,650,000

- Bonus depreciation: 100% on equipment placed in service after the Section 179 limit is applied

Here’s a simple version: buy a $120,000 piece of equipment, place it in service before December 31, 2026, and deduct the full $120,000 from taxable income that year. In a 30% tax bracket, that’s $36,000 saved at tax time.

Financing doesn’t block this deduction. Equipment can be financed and still qualify for the full Section 179 write-off, as long as it’s placed in service by year-end.

How to Qualify for Equipment Financing in 2026

Lenders weigh five factors:

- Credit score. Banks usually want 680 or higher. Lenders work with scores as low as 500 to 600, but charge more for the added risk.

- Time in business. Two years in business opens far more doors. Newer businesses still qualify, mostly through lenders or equipment-focused lessors.

- Annual revenue. Most lenders want revenue that covers the new payment several times over.

- Down payment. 10% to 20% is standard for loans. Many leases need nothing down.

- Equipment value and resale market. Lenders check whether the equipment holds value if they ever need to repossess and resell it.

The Federal Reserve’s 2025 Small Business Credit Survey looked at paperwork. Tax returns.

Bank statements. A clear purpose statement. Businesses that had these ready before applying saw higher approval rates. Notably higher. The full Federal Reserve report breaks this down by lender type and credit profile.

Community banks and credit unions deserve a closer look. Their credit thresholds often run lower than big national banks.

Their underwriting stays local too. A loan officer reviews the actual business. No automated score decides everything.

Take a small podcast production company. A large bank turned them down twice.

A local credit union approved them for a $45,000 camera and audio package. Why?

The loan officer sat down and reviewed their recurring sponsorship contracts in person. That review made the difference.

Equipment Financing for Small Businesses with Bad Credit

A low credit score doesn’t close every door. Options still open up, though the cost runs higher:

- Equipment-secured loans weigh the resale value of the asset more than a clean credit file, since the lender has the equipment as backup.

- Online and alternative lenders often accept scores in the 500s, paired with a larger down payment or a shorter term.

- Vendor financing through the equipment seller sometimes skips a hard credit pull altogether, especially for established dealers selling warehouse machinery or production gear.

- A co-signer or business partner with stronger credit can lower the rate significantly on a joint application.

The tradeoff is cost. A bad-credit equipment loan can run 20% to 35% APR, against 7% to 12% for a strong-credit borrower at a bank. Building six months of on-time payments, then refinancing, often saves thousands over the life of the deal.

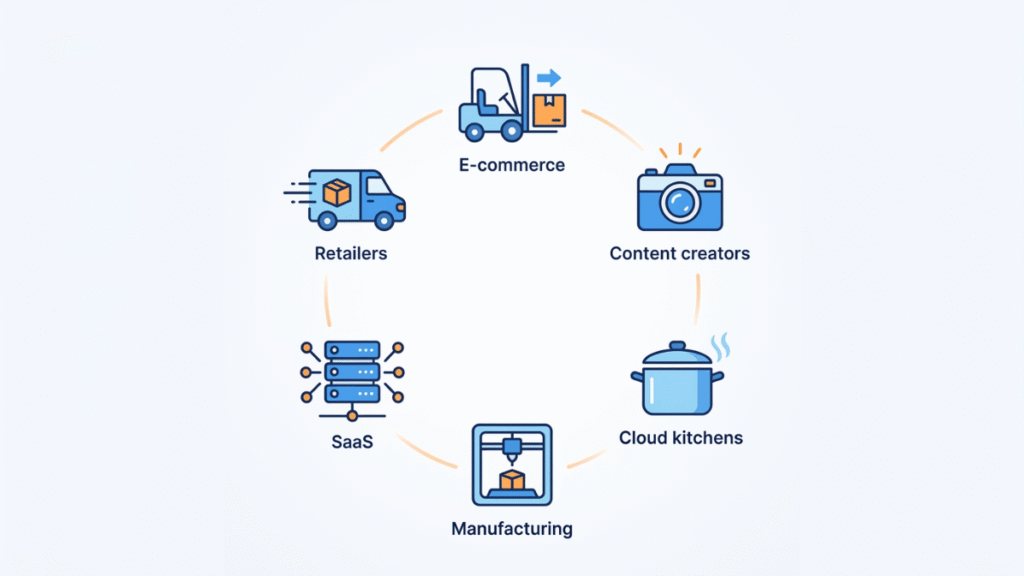

Equipment Financing for Small Businesses by Industry

The right lender and structure shifts depending on the type of business:

- E-commerce and fulfillment: Forklifts, conveyor systems, and packaging equipment dominate here. Banks lend more freely since this gear holds resale value well.

- Content creators, online coaches, and course creators: Cameras, lighting, and podcast or studio equipment usually fit a lease, since gear ages fast and creators tend to upgrade every two to three years.

- Cloud kitchens and ghost kitchens: Delivery-only food brands that sell through apps still need commercial ovens and prep equipment. Leasing wins often, since kitchen gear needs replacement every five to seven years.

- Print-on-demand and online manufacturing brands: DTG printers, embroidery machines, and 3D printers usually run through equipment loans, since the gear becomes a long-term production asset.

- SaaS and tech-enabled businesses: Servers and networking hardware sometimes qualify for equipment financing, though many tech businesses lease through their cloud provider instead of buying physical gear outright.

- Retailers running their own last-mile delivery: Delivery vans and route equipment usually fit SBA 504 loans or bank term loans, with longer terms matching the asset’s long working life.

Step-by-Step: How to Apply

- Get a quote on the equipment first. Lenders want the exact make, model, and price before they quote terms.

- Pull your credit report. Fix errors before applying, not after a denial.

- Gather your documents. Two years of tax returns, three to six months of bank statements, and a one-page summary of why you need the equipment.

- Compare at least three lenders. A bank, a credit union, and one lender gives a fair spread of rates and terms.

- Read the full term sheet. Check for prepayment penalties, balloon payments, and whether the rate is fixed or variable.

- Sign and confirm the funding timeline. Equipment loans close faster than real estate loans, often in one to two weeks through banks, and as fast as 24 to 48 hours through lenders.

A subscription snack box business almost signed a lease for her packaging line.

Buried on page six: a hidden $1,200 “equipment return fee.” She caught it. Why? She read every page before signing.

That one read saved her over a thousand dollars.

Equipment Loan vs. Equipment Lease

| Factor | Equipment Loan | Equipment Lease |

| Ownership | Yours after the final payment | Lender owns it during the term |

| Down payment | 10% to 20% typical | Often $0 |

| Monthly payment | Usually higher | Usually lower |

| Tax treatment | Section 179 and depreciation apply | Often deducted as a business expense |

| Best fit | Equipment used 5+ years | Equipment that ages fast |

| End of term | Asset is kept | Return, renew, or buy it out |

Neither option wins across the board. The right pick depends on how long the equipment stays useful and how cash flow looks month to month.

Common Mistakes That Slow Down Equipment Financing for Small Businesses

- Applying for the wrong loan size. Asking for too little leaves a gap for installation, delivery, or training costs.

- Skipping the rate comparison. A 22% rate against a 9% bank rate on a $100,000 loan adds up to tens of thousands in extra interest.

- Watching the monthly payment instead of the total cost. A low payment over 7 years can cost more than a higher payment over 4 years.

- Missing the Section 179 deadline. Equipment must be placed in service by December 31, not just ordered, to count for that tax year.

- Skipping the fine print on prepayment penalties. Some equipment loans charge a fee for paying off the balance early.

Final Thoughts

Equipment financing for small businesses comes down to three choices: loan or lease, bank or lender, now or later. The 2026 numbers favor owners who move with full paperwork ready, compare more than one lender, and place equipment in service before the Section 179 deadline.

The owners who come out ahead aren’t the ones with perfect credit. They’re the ones who read every page, ask every question, and pick the option that fits their cash flow, not just the lowest sticker rate.

FAQ

How fast can I get equipment financing for small businesses?

Lenders fund in 24 to 72 hours. Banks take one to three weeks. SBA loans often take three to eight weeks due to added paperwork.

Can a new business get equipment financing?

Yes. Many equipment lenders work with businesses open six months or longer, especially when the equipment itself holds strong resale value.

Does equipment financing affect personal credit?

Most lenders run a personal credit check during underwriting. Some report payment history to personal credit bureaus, especially for sole proprietors and small LLCs.

Is leasing or financing cheaper over time?

A loan usually costs less over the full life of the equipment, since payments build equity. A lease costs less upfront and avoids being stuck with outdated gear.

Can I refinance equipment financing for small businesses later?

Yes. Refinancing into a lower rate works the same as refinancing any secured loan, as long as the equipment still holds enough value to back the new loan.

What credit score do I need for an SBA equipment loan?

Most SBA lenders look for a personal credit score of 650 or higher, with the strongest terms going to scores above 700.

Aliza Khatun is a Digital Marketing Professional and the founder of DigiGenHub. She has helped various businesses grow their online presence through real-world experience in marketing, branding, traffic growth, and business strategy.

Through DigiGenHub, she shows how to build and grow a business from the ground up using Website Setup, SEO, Branding, Paid Promotion, and smart digital tools.

She also highlights how AI can be used to its full potential to make content creation, automation, marketing, and business growth faster and smarter.

She believes that the right knowledge, modern technology, and the right tools can help any individual or business build a stronger online presence.