Most startup founders put everything on a personal card at first. That feels easy. But it creates messy books, kills your tax deductions, and does nothing to build your company’s credit. Business credit cards for startups fix all three problems at once.

Why Startups Need a Dedicated Business Credit Card

A business card is not just a payment tool. It is a credit-building asset.

Getting a business credit card early pays off fast. It builds your company’s credit history.

It keeps personal and business expenses apart. It also covers cash gaps in those first shaky months.

The numbers back this up. The Federal Reserve Small Business Credit Survey 2026 found that 62% of businesses chose credit cards over loans in 2025. Founders want fast access to funds. Credit cards deliver that.

Let’s see what a business card does for a startup:

- Separates finances so tax time is clean and simple.

- Builds business credit with Dun & Bradstreet, Experian Business, and Equifax Business.

- Earns rewards on software, ads, travel, and office costs.

- Funds cash flow gaps between client payments.

- Adds employee cards with spending limits you control.

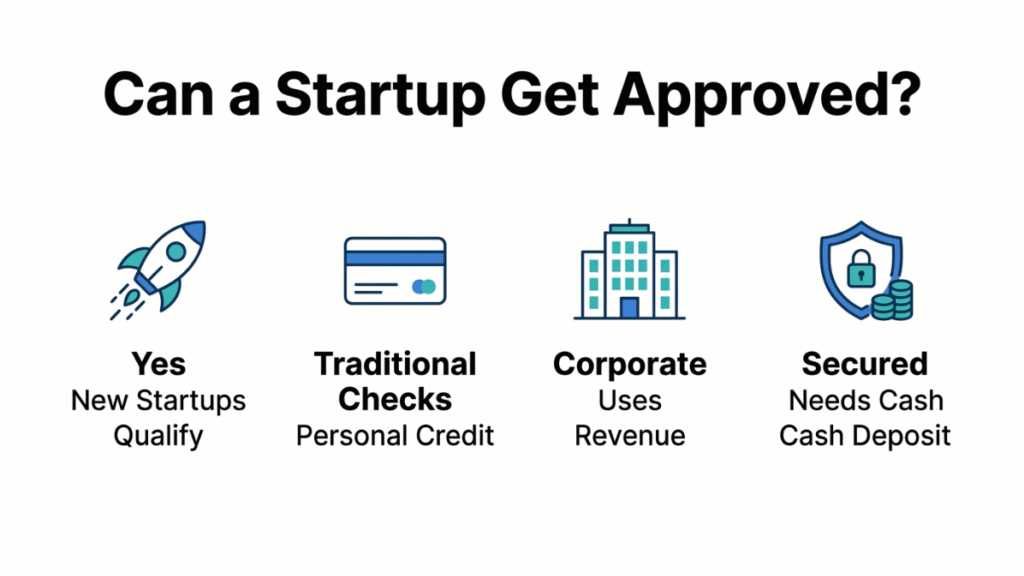

Can a Startup Actually Get Approved?

Yes. This was the hard part before. Today it is much more direct.

Business credit cards don’t require a minimum revenue or time in business. So you can apply even if your business is new and has no employees.

Startup founders have three clear paths to get a business credit card early on.

Traditional business credit cards check your personal credit profile. That is the most common starting point.

Corporate cards skip the credit score check. They look at your revenue or bank balance instead.

Secured business credit cards ask for a cash deposit upfront. That deposit becomes your credit limit.

What Issuers Look At

| Factor | Traditional Cards | Corporate/Fintech Cards |

| Personal credit score | Required (670+ typical) | Usually not required |

| Business revenue | Not required for most | Required or cash balance |

| Time in business | No minimum for most | Varies |

| Personal guarantee | Yes | Often no |

| Business bank account | Helpful | Usually required |

For a startup, approval is often based more on your personal credit than on your business’s financial track record. Many business credit cards look for a FICO Score around 670 or higher.

I worked remotely with a SaaS founder in Austin who applied for the Chase Ink Unlimited two days after registering her LLC.

She got approved based purely on her personal credit score of 710. Zero revenue. Zero business history. Card arrived in a week.

The 3 Types of Startup Business Cards

1. Traditional Business Credit Cards

Work like personal cards. Based on your personal credit. Carry a balance with interest. Best if you want flexibility on payments.

2. Corporate Charge Cards (Fintech)

No personal credit check. Based on your business bank balance or funding. Must pay in full each month. Best for funded startups.

3. Secured Business Cards

Require a cash deposit as collateral. Build credit from scratch. Best if personal credit is below 650.

Top Business Credit Cards for Startups

Below is an honest, practical comparison based on current terms. These are the cards founders actually use.

| Card | Best For | Annual Fee | Rewards | Approval Basis |

| Ink Business Unlimited | Overall/new businesses | $0 | 1.5% cash back on all purchases | Personal credit (680+) |

| Ink Business Cash | Office & tech spend | $0 | Up to 5% on office/internet/phone | Personal credit (680+) |

| Capital One Spark Cash Plus | High spenders | $150 (waived at $150K spend) | 2% unlimited cash back | Personal credit |

| Capital One Spark Classic | Fair/limited credit | $0 | 1% cash back | Personal credit (fair) |

| Brex Card | Funded startups, no personal guarantee | $0 | Up to 7x on rideshare, 4x travel | Business bank balance or revenue |

| Ramp Card | Spend management + no personal guarantee | $0 | 1.5% cash back | $25K+ in US business bank account |

| Amex Blue Business Plus | Everyday spend, no annual fee | $0 | 2x points on first $50K/year | Personal credit |

| U.S. Bank Triple Cash Rewards | 0% intro APR | $0 | 3% on gas, office, restaurants | Personal credit |

| Bank of America Secured | Bad credit/rebuilding | $0 | 1.5% cash back | Security deposit |

| Rho Corporate Card | Flexible qualification | $0 | Up to 1.5% cash back | Financial statements |

How to Pick the Right Card for Your Stage

This is where founders often overthink it. The right card depends on one thing: your current financial situation.

Pre-Revenue Startup

Go with a traditional card based on your personal credit. The Chase Ink Unlimited or Amex Blue Business Plus both have no annual fee and strong rewards.

A friend launched a consulting firm with zero clients at launch. She put her personal score (730) to work and got the Ink Business Unlimited on day one.

Within six months, she had a business credit profile showing on-time payments. That later helped her get a $50K line of credit from her bank.

Funded Startup (VC or Angel-Backed)

Two cards fit funded startups perfectly: Brex and Ramp.

Brex Card skips the credit check. No personal guarantee needed either. You need at least $50,000 in your business bank account if venture-backed.

Self-funded startups need $1 million. Hit that bar and you earn up to 7x points per dollar spent.

Ramp Card needs $25,000 in a US business bank account. It works for corporations, LLCs, and limited partnerships. Apply and get approved in under 48 hours. No annual fee at all.

Limited or Fair Personal Credit

The Capital One Spark Classic for Business is the best business credit card for a new business owner with no credit because it rewards with at least 1% cash back on all purchases and has a $0 annual fee.

Bad Credit

Go secured. If your personal credit is below 650, consider a secured business card. You’ll need to put down a deposit, but it lets you start building business credit immediately while your startup grows.

The 4-Step Approval Process (What Was Hard, Now Made Simple)

Before, founders burned hours filling out long applications, guessing what lenders wanted. Let’s learn exactly what to do.

Step 1: Get your EIN first

Get your EIN first. This gives your business its own identity with the IRS and is required for most business credit applications. Apply free at IRS.gov. Takes five minutes.

Step 2: Open a dedicated business bank account

Lenders like to see that you have a dedicated business account. It shows financial organization and separates your personal and business money.

Step 3: Apply for one card only

Don’t apply for multiple business cards at once. Get approved for one, use it responsibly for three to six months, then consider additional cards if needed. Multiple applications trigger hard pulls and hurt your score.

Step 4: If you have no revenue, enter $0

You can simply enter $0 in the revenue field on the application form if you have no business revenue yet. Most issuers let you use personal income to qualify.

How to Build Business Credit Fast

You can establish an initial business credit profile within three to six months of opening business accounts and using credit.

A Dun & Bradstreet PAYDEX score can be established in as little as 30 days once you have active trade lines reporting.

Building a strong business credit score typically takes 12 to 24 months of consistent, responsible use.

The fastest path:

- Get your EIN and business bank account open.

- Apply for one business credit card.

- Use it for regular business purchases (software, ads, subscriptions).

- Pay the full balance every month.

- Check your D&B, Experian Business, and Equifax Business reports every 90 days.

Paying in full avoids interest and signals to credit bureaus that you manage obligations well. This is the single most effective move for startup credit building.

Qualities to Check Before You Apply

Do not skip these. Small differences cost founders real money.

Annual Fee vs. Rewards

Start with a no-fee card. Most startups do not need a premium card yet. Only upgrade when your monthly spending makes the annual fee pay for itself.

Personal Guarantee

Most traditional cards tie you personally to the debt. If your business cannot pay, you pay.

Some fintech cards like Brex drop that requirement. But they set stricter business eligibility rules instead.

Charge Card vs. Credit Card

A charge card demands full payment every month. No carrying a balance. A credit card lets you pay a minimum and roll the rest forward. That flexibility comes with interest costs, though.

0% Intro APR

Need to buy equipment or software now without paying interest? The U.S. Bank Triple Cash Rewards gives you 0% APR for 20 months on new purchases. That is one of the strongest offers for startups right now. Check the latest terms at nav.com.

Rewards and Your Spending

Most startups burn money in the same few spots. Ads. Software. Contractors. Travel. Pick a card that rewards those exact categories. Flat-rate cash back keeps it simple. Category bonuses sound exciting but often miss where you actually spend.

Startup Credit Card Mistakes to Avoid

Mixing personal and business expenses

Every mixed transaction is a future bookkeeping headache and a missed deduction.

Carrying a balance on a high-APR card

Interest rates for business credit cards increased by 30.86% from Q1 2016 to Q1 2026. Pay in full every month.

Applying for too many cards at once

Each application triggers a hard pull. Space applications at least six months apart.

Ignoring your business credit reports

Errors go unnoticed and hurt your profile for years. Check regularly at Dun & Bradstreet, Experian Business, and Equifax Business.

One of my remote clients runs a Shopify dropshipping store in Texas. He carried a $12,000 balance on his business card for eight months.

The APR was 28%. He paid over $2,200 in pure interest. Not on inventory. Not on ads. Just interest.

A charge card would have forced him to clear the balance monthly. That one switch would have kept $2,200 in his business.

The Bottom Line

Choosing the right business credit cards for startups is straightforward. You just need to know where you stand.

Personal credit above 670? Start with Chase Ink Unlimited or Amex Blue Business Plus. Both are free. Both earn solid rewards.

Funded startup with cash in the bank? Go with Ramp or Brex. No personal guarantee. No credit check.

Credit below 650? Get a secured card. Use it for six months. Then upgrade.

The biggest mistake founders make is waiting. Every month without a card is a month your business credit score stays at zero. That costs you later when you need a loan or a lease.

Apply today. Pay the full balance every month. Within six months, your startup builds a credit profile that opens real doors.

FAQ

Can a brand-new LLC get a business credit card?

Yes. Your LLC can be one day old. That does not block you. You just need to be the owner or an authorized representative. Good personal credit does the heavy lifting at this stage.

Does applying affect my personal credit?

It can. Applying triggers a hard inquiry on your personal credit report. That may drop your score by a few points.

Nothing dramatic. Your payment history and credit utilization matter far more than one inquiry. Keep those clean and the impact stays small.

What if I am self-employed or a freelancer?

You still qualify. You do not need a registered business entity. Freelancers apply. Consultants apply.

Rideshare drivers apply. People selling on Amazon or Etsy apply. If you earn money independently, you can apply for a business credit card today.

Aliza Khatun is a Digital Marketing Professional and the founder of DigiGenHub. She has helped various businesses grow their online presence through real-world experience in marketing, branding, traffic growth, and business strategy.

Through DigiGenHub, she shows how to build and grow a business from the ground up using Website Setup, SEO, Branding, Paid Promotion, and smart digital tools.

She also highlights how AI can be used to its full potential to make content creation, automation, marketing, and business growth faster and smarter.

She believes that the right knowledge, modern technology, and the right tools can help any individual or business build a stronger online presence.