Your invoice says net 30. Your customer pays in 47 days. Payroll is due Friday.

This gap between billing and getting paid breaks more small businesses than slow sales ever could. You did the work. You sent the invoice. Now you wait.

Two tools fix this fast: invoice factoring and invoice financing. Both turn unpaid invoices into cash today instead of in 30, 60, or 90 days. The SBA working capital guide lists both as legitimate ways to free up money tied in unpaid invoices.

But invoice factoring vs invoice financing are not the same. One sells your invoice to someone else. The other borrows against it while you keep it.

That single difference changes who calls your customer, what shows up on your balance sheet, and what the cash costs you by the time it’s all paid back.

What Is Invoice Factoring?

Invoice factoring means you sell an unpaid invoice to a factoring company for upfront cash.

Let’s see how it works in four steps:

- You deliver a product or service and send a customer an invoice with normal payment terms (net 30, net 60, or net 90).

- You submit that invoice to a factoring company instead of waiting on payment.

- The factor checks your customer’s credit, not just yours, then pays you 70% to 95% of the invoice value within 24 to 48 hours.

- Your customer pays the factor directly, often after receiving a short notice letting them know where to send payment. Once that payment clears, the factor sends you the rest, minus its fee.

The factoring company now owns the invoice. It collects the money. It also takes on most of the risk if your customer pays late or never pays at all. This depends on whether your agreement is recourse or non-recourse (more on that below).

Most factors only buy B2B invoices from commercial customers, not invoices billed to individual consumers.

They also want clean paperwork: a signed contract or purchase order, proof of delivery, and an invoice with no liens already attached.

This setup makes invoice factoring a fit for newer businesses, or businesses with thin credit files, as long as their customers pay reliably.

Factors care more about your customer’s track record than your own. If your credit score is stopping you from getting funding, consider this option.

Compare it with other bad-credit funding solutions first. That way, you can choose the best fit before signing a long-term contract.

What Is Invoice Financing?

Invoice financing means you borrow money using your unpaid invoices as collateral.

You keep the invoice. You keep the customer relationship. You keep collecting payment the same way you always have.

Let’s learn the process:

- You send a customer an invoice as normal.

- You submit that invoice, or a batch of invoices, to a financing provider as collateral for an advance.

- The provider advances 80% to 95% of the invoice value, often within one to two business days.

- Your customer pays you directly, the same as before. You repay the advance plus a fee once that payment lands.

Your customer never finds out a financing provider is involved. This privacy is the biggest practical difference in invoice factoring vs invoice financing. And it matters a lot to businesses that work with the same clients for years.

Invoice financing is also called accounts receivable financing or invoice discounting.

Providers usually file a UCC lien on your receivables and want at least three to six months of business history along with steady monthly revenue.

Lenders look harder at your business credit here, since you stay responsible for collecting the money, not them.

Invoice Factoring vs Invoice Financing: The Core Differences

Side by side, the gap between these two tools is sharper than most people expect.

| Factor | Invoice Factoring | Invoice Financing |

| Who owns the invoice | The factoring company buys it | You keep ownership |

| Who collects payment | The factor contacts your customer | You collect, as usual |

| Customer awareness | Customer knows and pays the factor | Customer never knows |

| Credit focus | Mostly your customer’s credit | Often your business credit too |

| Balance sheet effect | Removed as a sale (FASB ASC 860) | Stays as an asset, with a linked liability |

| Typical advance rate | 70% to 95% | 80% to 95% |

| Typical cost | 1% to 5% per 30 days | 1% to 4% per month, plus interest |

| Funding speed | 24 to 48 hours per invoice | Same day to 2 business days |

| Best fit | Thin credit, strong customers | Established credit, wants privacy |

Notice the accounting line. Factoring counts as a true sale of a financial asset under standard accounting rules.

So the receivable leaves your books. Invoice financing works like a loan. Indeed, the receivable stays, with a matching liability sitting next to it. That detail matters if you’re tracking ratios for a future bank loan or investor pitch.

What You Need to Qualify

Qualification rules differ just as much as the cost structure does.

| Requirement | Invoice Factoring | Invoice Financing |

| Time in business | Often none required | Usually 3 to 6 months minimum |

| Minimum monthly invoicing | Varies by factor, often flexible | $10,000 to $15,000 or more |

| Invoice size minimum | $500 to $1,000 per invoice | $1,000 to $5,000 per invoice |

| Personal credit check | Soft check, rarely a blocker | Weighed alongside business credit |

| Paperwork needed | Invoice, proof of delivery, customer info | Bank statements, AR aging report, tax returns |

A brand-new company with one strong corporate client can often qualify for factoring on day one.

The same company would likely wait a few months and build a revenue track record before a financing provider says yes.

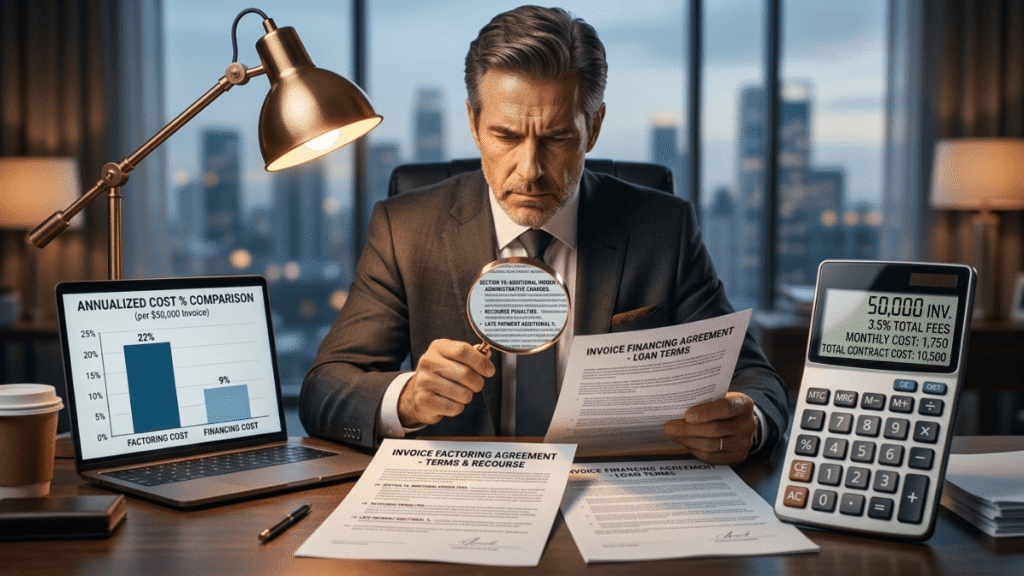

How Much Do Invoice Factoring and Invoice Financing Cost?

Both options quote a small percentage fee, which can hide a much higher annual cost. Here’s the math that uncovers it.

Invoice factoring example:

- Invoice value: $50,000

- Advance rate: 85%, so you get $42,500 upfront

- Factoring fee: 3% per 30 days, so $1,500

- Customer pays on day 30. You receive the remaining $6,000 ($50,000 minus $42,500 minus $1,500)

- Total received: $48,500 out of $50,000

Invoice financing example:

- Invoice value: $50,000

- Advance rate: 90%, so you get $45,000 upfront

- Financing fee: roughly 1% processing plus 0.5% per week for four weeks, near $1,000 total

- Customer pays on day 30. You receive the remaining $4,000 ($50,000 minus $45,000 minus $1,000)

- Total received: $49,000 out of $50,000

Both deals can also carry extra charges worth asking about upfront: an origination fee, a monthly minimum volume fee, and a small ACH or wire fee per draw. None of these show up in the headline rate, so confirm them before you sign.

The numbers above look close on a single invoice. They stop looking close once you annualize them. Use this formula to compare any offer fairly:

Annualized cost ≈ (fee percent ÷ days outstanding) × 365

A 3% fee over 30 days works out to roughly 36% on an annual basis. A 1.5% fee over 30 days comes to about 18%.

A Federal Reserve report on small business lending flagged this exact problem. It noted that a factor rate of 1.15 can hide an undisclosed APR near 70%.

This happens because small business credit products do not follow the same disclosure rules as consumer loans.

Always ask for the annualized number before comparing invoice factoring and invoice financing offers side by side. The percentage on the page rarely tells the whole story.

Types of Invoice Factoring and Financing Options

Not every factoring or financing deal works the same way. The structure you pick changes your cost and your risk just as much as the basic choice between selling and borrowing.

| Option | How It Works | Best For | Typical Cost |

| Recourse factoring | You stay responsible if your customer never pays | Reliable, creditworthy customers | Lower fees, 1% to 3% per 30 days |

| Non-recourse factoring | The factor absorbs the loss on customer default | A shaky or unfamiliar customer | Higher fees, 2% to 5% per 30 days |

| Spot factoring | You factor a single invoice, no ongoing contract | Occasional cash gaps | Higher per-invoice fee, no minimum |

| Whole ledger factoring | You factor your full accounts receivable book | Steady, high invoice volume | Lower per-invoice fee, contract required |

| Confidential invoice discounting | You borrow against invoices, customer never knows | Protecting long-term client trust | 1% to 3% plus interest |

| Asset-based line of credit | A revolving line secured by your full ledger | Established businesses, $1M+ in receivables | Lowest overall cost |

Recourse factoring costs less because the factor takes on less risk. Non-recourse costs more but protects you if a customer goes under.

Spot factoring gives flexibility with no long-term commitment, though you pay a premium for that freedom.

Whole ledger deals reward volume with lower per-invoice fees. Your customer concentration plays a role too: if one client makes up most of your receivables. Expect tighter terms or a request for non-recourse coverage on that account specifically.

Which Option Fits Your Business?

Run through these five questions before you choose between invoice factoring and invoice financing.

- Is your own business credit weak? Factoring leans on your customer’s credit, so it works even with a thin or damaged file. Financing usually checks your business too.

- Do you want your customers calling you, not a stranger? Financing keeps that relationship private. Factoring puts a third party in the conversation.

- Do you have staff to chase down late payers? Factoring hands that job to someone else. Financing leaves it with your team.

- Does your balance sheet need to look clean for a future loan or investor? Factoring removes the receivable as a sale. Financing adds a liability next to it.

- How many invoices do you need funded each month? High, steady volume often qualifies for whole ledger deals with lower fees on either side.

A marketing agency owner I advised had exactly one weak point: a personal bankruptcy from eight years back that still showed on his report.

His clients were large national brands that always paid within 35 days. Factoring matched his situation.

The factor cared about his clients’ payment history, not his old bankruptcy filing.

If your answers point the other way (strong business credit, a need for privacy, a customer base that would notice a stranger collecting payment), invoice financing usually wins.

This decision also connects to your bigger funding picture. If invoice factoring vs invoice financing still leaves a gap, compare it against other loans for small businesses or a revenue-based financing structure. That ties repayment to your monthly sales instead of a single invoice.

Invoice Factoring vs Invoice Financing: What’s New in 2026

Three shifts are reshaping this market right now.

First, the global numbers keep climbing. Worldwide factoring turnover passed €4 trillion in 2025.

That was a 3.7% increase from 2024, according to global factoring statistics from the industry’s main reporting body. The Americas recorded some of the strongest growth.

Part of this growth comes from e-invoicing mandates and digital registries. These tools help factors verify invoices faster. They also make it easier to fund invoices quickly.

Second, the US picture looks different from the global one. Per US market size data, down 1.9% for the year, as more small businesses shift toward invoice financing, lines of credit. Also, fintech tools that pull receivables data straight from accounting software.

Third, AI-driven underwriting is cutting approval times across both products. Providers now pull bank data, invoice history, and customer payment patterns in minutes instead of days. this shrinks that earlier 3 to 10 day setup window for new accounts.

None of this changes the core math. Cash flow still matters more than ever. According to the Small Business Credit Survey, only 42% of financing applicants got the full amount they asked for in 2025. And 22% got nothing at all. Both tools remain among the fastest ways to close that gap without waiting on a bank’s full approval cycle.

Common Mistakes That Cost You Money

A few patterns show up again and again with businesses that pick the wrong structure or skip the fine print.

- Choosing tiered pricing without reading the schedule. Tiered fees start low and climb every 10 to 15 days the invoice stays unpaid. A flat fee often costs less if your customers tend to pay late.

- Ignoring the reserve holdback. Factors typically hold back 5% to 30% of the invoice until your customer pays. Plan your cash needs around the advance, not the full invoice value.

- Forgetting to ask about recourse or non-recourse. Recourse deals leave you on the hook if a customer defaults. That detail belongs in your contract review, not a surprise six weeks later.

- Comparing fee percentages without annualizing them. A 2% fee for 15 days costs more per year than a 4% fee for 60 days. Run the math from the cost section above on every quote.

- Overlooking customer concentration limits. Most factors cap exposure to a single customer at 25% to 40% of total receivables. If one client makes up most of your invoices, ask about this before you apply.

- Treating the advance as a fix for spending habits. A funding tool closes a timing gap. It doesn’t fix a deeper problem with how you manage small business cash flow elsewhere in the business.

How to Apply: Step-by-Step

- Gather your documents. Most providers want 3 to 6 months of bank statements, an accounts receivable aging report, a year or two of tax returns, and sample invoices.

- Check your customer concentration. List your top customers by percentage of total receivables. Flag anything above 25%.

- Request quotes from at least three providers. Ask each one for the advance rate, the fee structure (flat or tiered), the reserve holdback, and whether the deal is recourse or non-recourse.

- Run the annualized cost formula on every quote. Compare offers fairly before signing anything.

- Confirm setup time and per-invoice funding time separately. Setup often takes 3 to 10 business days. Funding per invoice should land in 24 to 48 hours for factoring or 1 to 2 days for financing once you’re approved.

- Read the termination clause. Some contracts lock you in for 6 to 12 months with an early exit fee. Know that number before you sign.

Final Take

Pick invoice factoring if your own credit is shaky. But your customers pay reliably, and you’d rather hand off collections entirely.

Pick invoice financing if your business credit is solid, you want to keep your customer relationships private, and your team already handles collections well.

Either way, you’re solving the same problem: turning a 30, 60, or 90-day wait into cash you can use this week. The right pick comes down to your credit profile, your need for privacy, and how the deal will look on your books a year from now. If neither tool fits, weigh a business loan vs crowdfunding before you lock into a receivables contract.

Run the annualized math on every offer. Check whether it’s recourse or non-recourse.

Confirm the reserve holdback before you count on the full invoice value. Invoice factoring vs invoice financing gets simple once you know what to ask.

FAQ

Is invoice factoring considered debt?

No. Factoring is a sale of an asset, not a loan, so it doesn’t add debt to your balance sheet. Invoice financing does add a liability, since it works like a loan.

Can a startup with no credit history use invoice factoring?

Yes. Factors mainly check your customer’s credit, not your business history, which makes factoring accessible to brand-new companies with established commercial clients.

Do invoice factoring companies check personal credit?

Some run a soft check, but it rarely blocks approval if your customers have strong payment records. Invoice financing providers tend to weigh personal and business credit more heavily.

What happens if my customer never pays the invoice?

Under a recourse agreement, you repay the advance. Under a non-recourse agreement, the factor absorbs that loss, though non-recourse deals usually cost more upfront.

Can I switch from invoice factoring to invoice financing later?

Yes, once your business credit improves or you want more control over collections. Most providers allow this switch between contract terms, not mid-contract.

Does invoice factoring hurt customer relationships?

It can, if your customer is unfamiliar with the practice. A short heads-up call before the factor reaches out usually smooths this over.

Is invoice financing reported to business credit bureaus?

Sometimes. It depends on the provider and whether the advance is structured as a loan or a line of credit. Ask directly before signing.

What industries use invoice factoring the most?

Staffing, trucking, manufacturing, construction, and healthcare services lead usage, mostly because they deal with long payment terms and steady B2B billing.

Can I factor international invoices?

Yes, though international factoring usually carries higher fees and stricter documentation, since cross-border collection adds risk and complexity.

How fast can I get my first advance after signing up?

Setup usually takes 3 to 10 business days. Once approved, your first invoice typically funds within 24 to 48 hours for factoring or 1 to 2 business days for financing.

Aliza Khatun is a Digital Marketing Professional and the founder of DigiGenHub. She has helped various businesses grow their online presence through real-world experience in marketing, branding, traffic growth, and business strategy.

Through DigiGenHub, she shows how to build and grow a business from the ground up using Website Setup, SEO, Branding, Paid Promotion, and smart digital tools.

She also highlights how AI can be used to its full potential to make content creation, automation, marketing, and business growth faster and smarter.

She believes that the right knowledge, modern technology, and the right tools can help any individual or business build a stronger online presence.