Choosing between a business loan vs crowdfunding can feel confusing at first. Both bring money in.

But they work very differently. The wrong choice costs you months and money. This guide cuts through the noise. You get clear differences, current numbers, and a straight path forward based on your situation.

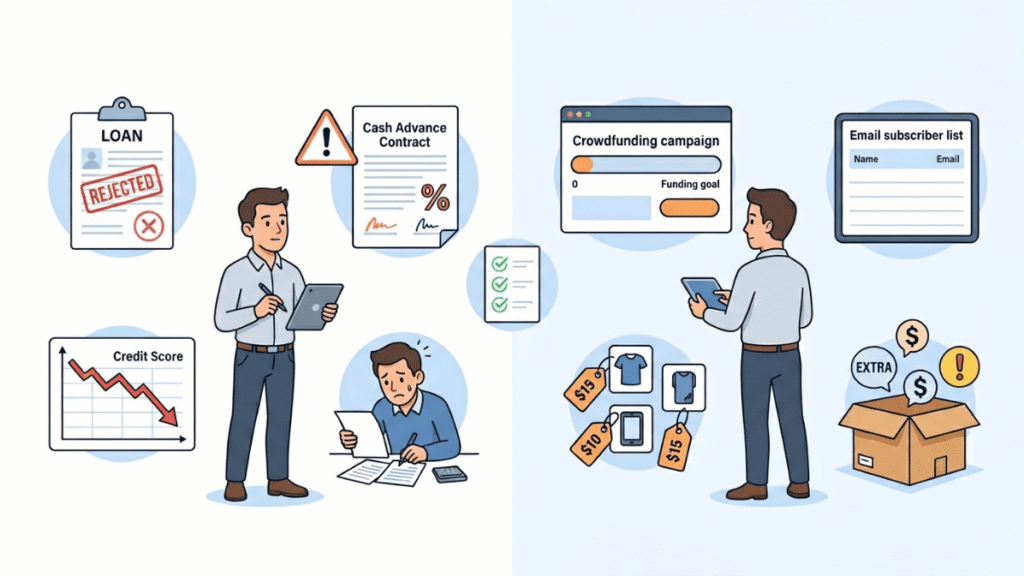

Business Loan vs Crowdfunding

Picking between a business loan vs crowdfunding comes down to three things: your credit, your stage, and your goal size.

Need over $100K with a solid credit history? A business loan wins. Need to test a product idea with zero credit history? Crowdfunding gets you there faster.

Loans give you large capital with predictable repayments. Crowdfunding builds your audience while filling your account. Both have fees. Both have risks. Neither is perfect alone.

The move most founders miss? Use both. Run a crowdfunding campaign first. Then take that proof straight to a lender.

In 2026, funding is not one-size-fits-all. Your situation decides your path.

Start with your numbers. Check your credit. Set your goal. Then pick the path that fits where your business stands today.

Business Loan vs Crowdfunding: Full Comparison

| Factor | Business Loan | Crowdfunding |

| Typical amount | $10K to $5M+ | $1K to $100K |

| Repayment | Monthly with interest | None (rewards/equity varies) |

| Credit score needed | 620–680+ | Not required |

| Time to funds | 2–8 weeks | 30–60 days (campaign period) |

| Collateral required | Often yes | No |

| Business age required | 2+ years (most lenders) | Pre-revenue accepted |

| Platform or origination fee | 1–5% origination | 5–8% platform + 3–5% payment |

| Ownership dilution | None | Possible (equity model) |

| Marketing benefit | None | High (public visibility) |

| Failure consequence | Credit damage, collateral loss | No funds released (all-or-nothing) |

| Best stage | Established business | Early stage or pre-revenue |

The Cost Comparison

This is where people get surprised. Business loans have interest. Crowdfunding has platform fees plus the cost of fulfilling rewards.

Business loan cost example:

- Loan amount: $100,000

- Interest rate: 10.5% (SBA average, 2025)

- Term: 5 years

- Total repaid: approximately $128,000

Rewards crowdfunding cost example:

- Goal: $30,000 raised on Kickstarter

- Platform fee (5%): $1,500

- Payment processing (3–5%): $900 to $1,500

- Reward fulfillment (product + shipping): $8,000 to $12,000

- Net received: roughly $16,000 to $20,000

That gap is real. Many first-time campaigners forget to budget fulfillment costs. They raise $30K and walk away with $14K after all expenses. Plan your reward tiers carefully before you launch.

Why You Shouldn’t Ignore This Decision in 2026

Interest rates stayed high through late 2025. Banks tightened lending standards for small businesses.

At the same time, U.S. crowdfunding crossed $1.7 billion in total project funding in 2025. Statista’s Crowdfunding Report 2026.

More founders now treat crowdfunding not just as fundraising but as a product launch strategy.

So the business loan vs crowdfunding question is no longer purely financial. It is also a marketing and timing decision.

What a Business Loan Actually Requires

Most people apply for a loan without checking if they qualify. Let’s see what lenders check in now:

- Credit score: 620 minimum for SBA loans, 680+ for traditional banks

- Time in business: Most banks want 2 full years of operation

- Annual revenue: Banks typically want at least $100K in documented revenue

- Debt service coverage ratio: Your cash flow must cover 1.25x the loan payment

- Collateral: Many lenders require assets to back the loan

The SBA 7(a) loan remains the most popular government-backed option. The average approved loan in fiscal year 2025 was $538,000, per the SBA FY2025 Annual Report. Approval takes 2 to 8 weeks depending on your lender and paperwork.

For newer businesses with lower credit scores, SBA microloans go as low as $500.

Community Development Financial Institutions (CDFIs) offer more flexible terms for underserved areas. Find a CDFI near you.

What Crowdfunding Actually Requires

Crowdfunding has no credit check. No collateral. No bank approval. But it has its own hard requirements that people miss.

The three types you need to know:

1. Rewards-based crowdfunding (Kickstarter, Indiegogo)

You offer backers a product or perk in exchange for pledges. Best for physical products and creative projects.

Kickstarter uses an all-or-nothing model. You only receive funds if you hit your goal.

2. Equity crowdfunding (Wefunder, Republic)

Investors get a stake in your company. You raise larger amounts but give up partial ownership.

The SEC’s Regulation Crowdfunding allows companies to raise to $5 million per year this way.

3. Donation-based crowdfunding (GoFundMe)

No repayment, no perks required. Better for community or social causes than for-profit businesses.

What most campaigns get wrong

They launch with no audience. The top 10% of Kickstarter campaigns have a built email list before day one.

Campaigns with 30 backers in the first 48 hours are 4x more likely to succeed, according to Kickstarter’s own stats.

A small online apparel startup I advised used Indiegogo’s flexible funding model. They set a $15,000 goal and raised $41,000.

They used the excess to negotiate bulk fabric pricing. They had zero revenue before the campaign. Crowdfunding gave them both capital and their first real customers at once.

Top Crowdfunding Platforms Compared

| Platform | Best For | Model | Fee | Success Rate |

| Kickstarter | Products, creative projects | Rewards (all-or-nothing) | 5% + 3–5% payment | ~40% |

| Indiegogo | Tech, flexible campaigns | Rewards or flexible funding | 5% + 3% payment | ~17% |

| Wefunder | Startups seeking investors | Equity | 7.5% of raised amount | Varies |

| Republic | Mission-driven startups | Equity or revenue share | 6% + 2% in securities | ~30% (selective) |

| GoFundMe | Community or social causes | Donation | 0% platform + 2.9% payment | N/A (no goal lock) |

Platform fees verified from official pricing pages, June 2026.

When to Pick a Business Loan

Choose a business loan when:

- You need more than $100,000

- Your credit score is above 650

- Your business has 2 or more years of history

- You want to keep full ownership

- You need predictable, lump-sum capital for equipment or expansion.

Also check how to improve your business credit score before applying. A better score directly lowers your interest rate and improves your approval chances.

When to Pick Crowdfunding

Choose crowdfunding when:

- You have a physical product people can see and want

- You have no business credit history

- You want to validate demand before manufacturing

- You want to build an audience while raising money

- You cannot qualify for a loan right now

The crowdfunding market grew 11.4% in the U.S. from 2024 to 2025. Tech gadgets, sustainability products, and food innovations top the categories in 2026, per Massolution’s Crowdfunding Industry Report. Campaigns with video pitches raise 114% more on average than those without.

The Hidden Power of Using Both

Here is the strategy most guides skip. You do not have to choose just one.

The stair-step method:

Step 1: Launch a crowdfunding campaign first. Raise initial capital. Collect backer data and revenue receipts.

Step 2: Use raised funds and campaign results as proof of concept. Banks increasingly accept crowdfunding history as soft market validation.

Step 3: Apply for a business loan with your campaign data attached. A successful campaign shows cash flow potential and an existing customer base.

Lenders like Accion Opportunity Fund and Kiva U.S. explicitly support post-crowdfunding loan applicants. Check Accion Opportunity Fund to see if you qualify.

Common Mistakes to Avoid

With business loans:

- Applying at a big bank first when a credit union or CDFI approves faster

- Not checking your personal credit score before applying

- Taking a merchant cash advance instead of a proper loan (effective rates often exceed 100%)

- Borrowing more than your cash flow can support at 1.25x the payment

With crowdfunding:

- Setting your goal too high (only raise what you genuinely need)

- Launching with no email list or social following

- Underpricing rewards to seem generous (this kills your margin)

- Ignoring international shipping costs in your budget

- Forgetting that crowdfunding income may be taxable as ordinary business income

Which Funding Path Fits Your Situation?

| Your Situation | Better Choice | Reason |

| Need $250K+, have credit history | Business loan | Banks fund large amounts reliably |

| Pre-revenue, physical product idea | Crowdfunding | No credit needed; test demand first |

| Want investors, not debt | Equity crowdfunding | Raise without repaying; gain community |

| Established business, need working capital | Business loan | Predictable repayment, full ownership kept |

| Low credit score, early stage | Crowdfunding first | Build traction, then qualify for a loan |

| Need funding plus brand exposure | Crowdfunding | Campaign builds audience and media coverage |

| Minority or underserved business owner | CDFI loan | Flexible terms, lower credit bar |

If you are also evaluating equity-based options, read more about equity financing for small businesses before committing to a crowdfunding type.

Final Take

The business loan vs crowdfunding debate has no single right answer. It depends on your stage, product type, credit history, and goal size. Loans give you large, reliable capital with no public campaign required. Crowdfunding gives you community, validation, and funding without any credit check.

In 2026, the best founders do not pick sides. They sequence. Crowdfund first to prove demand. Use that proof to unlock loan capital. That combination beats either path alone.

Start with your numbers. Know your credit score. Know your goal amount. Know your timeline. The right funding path becomes clear once you do.

FAQ

Can I use crowdfunding income as proof of income on a loan application?

Yes, but it depends on the lender. Some CDFIs and SBA-approved lenders accept documented crowdfunding revenue.

Bring your campaign receipts, payout statements from the platform, and bank deposit records. Traditional banks are stricter. Online lenders like Bluevine are more flexible. Always confirm with the lender before you apply.

What happens to backers if my campaign fails after I collect the money?

On Kickstarter, you only collect funds after hitting your goal. If you miss the goal, no money changes hands. On Indiegogo with flexible funding, you keep whatever you raise even if you miss the goal. If you then fail to deliver rewards, backers can report you to the platform and may pursue legal action. Document every communication and delay carefully.

Will a rejected loan application hurt my credit score?

A hard credit inquiry drops your score by roughly 2 to 10 points. Multiple hard pulls within 14 to 45 days count as one inquiry in most scoring models.

The rejection itself does not lower your score. Applying repeatedly over months does the damage. Check your score first at AnnualCreditReport.com before submitting any application.

Are there AI tools in 2026 that help you choose between a loan and crowdfunding?

Yes. Nav connects business owners to loan options based on their credit profile. Lendio uses an AI-matching engine across 75+ lenders.

On the crowdfunding side, Krowdster uses data to predict campaign success before you launch. These tools save time and reduce poor application decisions. None of them replace a financial advisor for large amounts.

Can a non-U.S. founder run a crowdfunding campaign targeting U.S. backers?

Yes. Kickstarter is available in 25+ countries. Indiegogo is fully global. You do not need to be U.S.-based to raise from U.S. backers.

However, equity crowdfunding under SEC Reg CF is limited to U.S.-registered companies. For rewards campaigns, you need a valid bank account in a supported country and a legal entity to receive funds.

Does crowdfunding success help you qualify for a business loan faster?

It can. A completed campaign with documented revenue, a customer base, and bank deposit records strengthens a loan application.

CDFIs and alternative lenders weigh this evidence seriously. Traditional banks care less about campaign history and more about your credit score and tax returns. The strongest applications combine both.

What is the minimum audience size before launching a crowdfunding campaign?

Most experienced campaign coaches recommend at least 500 engaged email subscribers before launch day.

That pre-launch list drives the first 30% of your goal in the first 48 hours. That early momentum signals to the platform algorithm to feature your campaign.

Building a waitlist page 60 days before launch is the most effective way to grow that list.

Are business loan interest rates expected to drop in late 2026?

The Federal Reserve held rates steady in early 2026 after modest cuts in late 2025. SBA loan rates currently sit between 10.5% and 13% depending on loan size and term.

Most projections point to small decreases in late 2026 if inflation stays below 3%.

A 1 to 2% rate drop on a $100K loan saves $1,000 to $2,000 per year. That is rarely worth delaying your business growth by 12 months. Track updates at FederalReserve.gov.

Can I run a crowdfunding campaign and apply for a loan at the same time?

Yes. There is no rule against it. Running both in parallel can actually strengthen your position.

Use the crowdfunding campaign to cover immediate costs and generate market proof. Apply for the loan simultaneously.

If the loan closes first, use the funds together. Just make sure your total funding does not exceed what your business plan justifies. Lenders will ask about all incoming capital sources.

Aliza Khatun is a Digital Marketing Professional and the founder of DigiGenHub. She has helped various businesses grow their online presence through real-world experience in marketing, branding, traffic growth, and business strategy.

Through DigiGenHub, she shows how to build and grow a business from the ground up using Website Setup, SEO, Branding, Paid Promotion, and smart digital tools.

She also highlights how AI can be used to its full potential to make content creation, automation, marketing, and business growth faster and smarter.

She believes that the right knowledge, modern technology, and the right tools can help any individual or business build a stronger online presence.